Understanding the Right Entity Structure: Kabushiki Kaisha vs. Goudou Kaisha vs. Branch

Key Takeaways

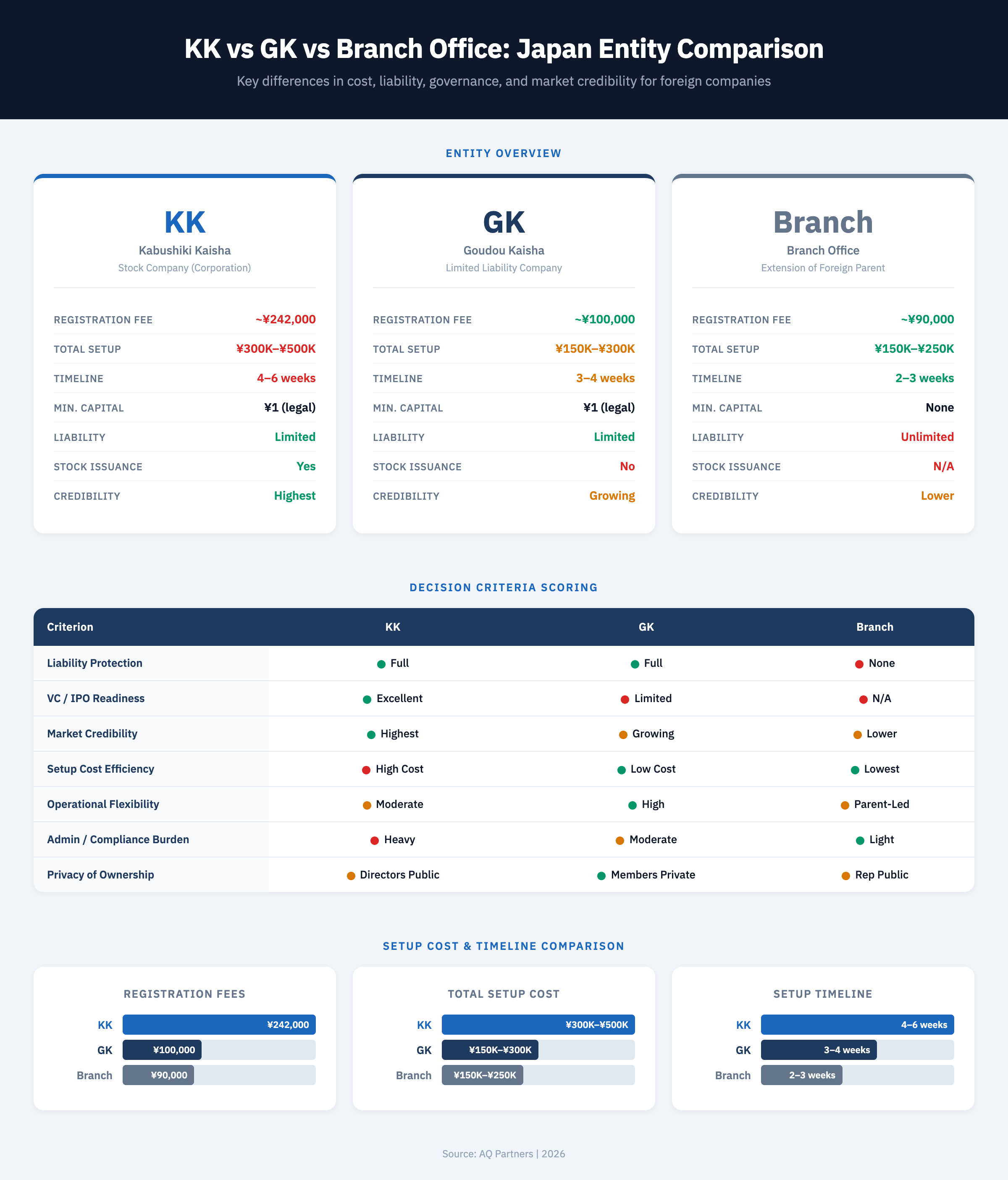

- A Kabushiki Kaisha (KK) provides the highest market credibility and is required for stock issuance or IPO paths — registration costs approximately ¥242,000 and setup takes 4-6 weeks, but the structure is strongly preferred by traditional Japanese corporations, banks, and government entities.

- A Goudou Kaisha (GK) offers limited liability at roughly half the setup cost of a KK — registration fees are approximately ¥100,000, governance requirements are minimal, and major companies including Apple Japan and Amazon Japan operate as GKs, demonstrating broad market acceptance.

- A branch office is the fastest and cheapest option but exposes the parent company to unlimited liability — registration fees are approximately ¥90,000 and setup takes 2-3 weeks, making branches suitable for market testing, but the parent bears full legal responsibility for all branch obligations.

- All three structures face the same corporate tax rates of approximately 30-34% on Japan-sourced income — the choice between KK, GK, and branch does not change the headline tax rate, though branches face more complex transfer pricing requirements and profit allocation rules.

- The minimum capital requirement for both KK and GK was eliminated in 2006 under the Companies Act — while the legal minimum is ¥1, most foreign companies capitalize at ¥5-10 million to satisfy bank account opening requirements and demonstrate operational viability to Japanese partners.

Understanding Japan's Business Entity Types

Japan's Companies Act provides three principal structures for foreign companies establishing operations in the country: the Kabushiki Kaisha (KK, or stock company), the Goudou Kaisha (GK, or limited liability company), and the branch office (an extension of the foreign parent entity). Each structure carries different implications for liability, governance, cost, and market perception.

For foreign companies entering Japan, entity selection is one of the first and most consequential decisions. According to JETRO's business setup guide, the registration process, capital requirements, and ongoing compliance obligations differ substantially between entity types. The structure you choose will affect everything from opening a corporate bank account to hiring employees and entering contracts with Japanese partners.

Japan's 2006 Companies Act reform eliminated minimum capital requirements for both KK and GK formations and introduced the GK as a new entity type modeled on the American LLC. Under the Companies Act (Act No. 86 of 2005), both domestic and foreign investors can establish any of these structures, though practical considerations around liability, cost, and credibility typically narrow the decision. For a broader overview of regulatory and operational requirements beyond entity selection, see our comprehensive market entry guide.

Kabushiki Kaisha (KK): The Standard Corporation

A Kabushiki Kaisha is Japan's stock company structure, equivalent to a corporation in the United States or a public limited company in the United Kingdom. It is the most established and widely recognized business entity in Japan.

The KK has been the backbone of Japanese business for decades. When Japanese companies are listed on stock exchanges, they are almost exclusively structured as Kabushiki Kaishas. This familiarity makes the KK instantly recognizable and respected in the Japanese business community. According to JETRO, the KK remains the dominant structure among large enterprises and publicly listed firms in Japan.

Governance and Structural Requirements

A KK requires at least one director. There is no requirement for the director to be a Japanese national or resident, though having local representation is often practical. For companies with capital exceeding certain thresholds or meeting other criteria under the Companies Act, a board of directors and auditors may be required.

Shareholders hold clear ownership rights, and shares can be transferred, making this structure suitable for companies seeking outside investment or planning an eventual public listing. The KK requires regular shareholder meetings and proper documentation of major corporate decisions. These governance requirements translate to higher ongoing professional fees for accounting and legal compliance.

Capital and Formation Costs

Prior to 2006, establishing a KK required minimum capital of ¥10 million. The Companies Act reform eliminated this requirement. Today, a KK can be established with ¥1 of capital, though most businesses opt for more substantial capitalization to demonstrate credibility. Registration and licensing taxes total approximately ¥242,000, which includes ¥150,000 in registration license tax (or 0.7% of capital if higher) and approximately ¥52,000 in notarization fees for the articles of incorporation. Total formation costs, including professional services, typically range from ¥300,000 to ¥500,000.

Advantages

The primary advantage is credibility. Many established Japanese companies, government agencies, and financial institutions strongly prefer to work with KKs. For businesses planning to raise capital, the ability to issue different classes of shares and the familiar corporate structure make it easier to attract investors. The KK also provides structural flexibility for growth, accommodating additional shareholders, directors, and complex governance arrangements without fundamental restructuring.

Disadvantages

The formality of the KK creates a higher administrative burden. Reporting requirements, bookkeeping obligations, and professional fees are all greater than for other structures. Initial setup costs are the highest among the three options, and the registration process typically takes 4-6 weeks to complete. After incorporation, companies must complete post-incorporation filings with tax offices, labor bureaus, and social insurance agencies.

When a KK Makes Sense

A KK is typically the right choice for significant, long-term operations in Japan, particularly when dealing with traditional Japanese corporations, government entities, or financial institutions. It is the preferred structure for companies planning to seek investment from Japanese venture capitalists or eventually pursuing a public listing. Companies in regulated industries or those requiring specific licenses often find that a KK is expected or even required.

Goudou Kaisha (GK): The Flexible Alternative

The Goudou Kaisha is Japan's limited liability company, introduced in 2006 as part of corporate law reforms. It offers a simpler, more flexible, and more cost-effective alternative to the KK while still providing limited liability protection.

Despite being a newer structure, the GK has gained significant acceptance among foreign companies. Major companies including Apple Japan, Amazon Japan, and Google Japan operate as GKs, helping to legitimize this structure. According to JETRO's entity comparison guide, the GK is increasingly popular among foreign-owned subsidiaries that do not require stock issuance or public listing capability.

How the GK Differs from a KK

The fundamental difference lies in governance and flexibility. A GK is member-managed rather than shareholder-managed. Members hold membership interests instead of shares, and they have direct control over operations. Profit distributions and management responsibilities can be structured flexibly through the articles of incorporation, without needing to match capital contribution ratios.

Unlike a KK, a GK does not issue stock, making it unsuitable for companies planning to raise external capital or go public. Governance requirements are simpler: no board of directors, no auditors, and no mandatory shareholder meetings. Major decisions can be made by member consensus according to the rules established in the formation documents.

Formation Costs and Requirements

The GK's registration and licensing tax is approximately ¥100,000 (or 0.7% of capital if higher), less than half the cost of establishing a KK. The GK also does not require notarization of articles of incorporation, saving approximately ¥52,000 compared to a KK. Total formation costs typically range from ¥150,000 to ¥300,000, including professional services.

Advantages

Cost efficiency is the GK's primary advantage. Both formation and ongoing administrative costs are lower than a KK. The simpler governance structure means less complex bookkeeping, fewer mandatory filings, and lower professional fees. The GK also offers operational flexibility: profit distributions can be structured based on factors other than capital contribution, and management decisions can be made more quickly. Privacy is another benefit, as member information does not need to be publicly registered.

Disadvantages

Some traditional Japanese companies and institutions still view GKs as less prestigious than KKs. If you need to raise capital from outside investors or go public, you will need to convert to a KK, which involves additional costs and administrative work. The GK structure may be less familiar to some Japanese accountants and lawyers, though this is diminishing as GKs become more common.

When a GK Makes Sense

A GK is often ideal for foreign companies establishing a wholly-owned subsidiary. It is particularly attractive for smaller operations, early-stage market entries, direct-to-consumer businesses, e-commerce companies, and organizations working primarily with international partners. For companies primarily focused on hiring employees in Japan, an Employer of Record (EOR) arrangement may be worth considering as an alternative. Service businesses, consulting firms, and technology companies often find the GK structure perfectly adequate, especially when cost efficiency and operational flexibility are priorities.

Branch Office: Operating Without a Separate Entity

A branch office is not a separate legal entity but an extension of the foreign parent company registered to operate in Japan. It can conduct business activities, but it remains legally inseparable from the parent organization.

Establishing a branch requires registering with the Legal Affairs Bureau and appointing a representative in Japan authorized to act on behalf of the parent company. The registration process is generally simpler than incorporating a new entity. Registration fees are approximately ¥90,000, and total costs including professional services typically range from ¥150,000 to ¥250,000. However, you must submit certified copies of the parent company's articles of incorporation and corporate registry certificates, properly translated into Japanese and notarized, which adds complexity.

Liability and Tax Considerations

The critical issue with a branch is liability. Because the branch is not a separate legal entity, the parent company is fully liable for all obligations incurred by the Japanese branch. Creditors can pursue the parent company's global assets for branch debts.

From a tax perspective, branches are taxed on Japan-sourced income at the same corporate rates as KKs and GKs, typically ranging from approximately 30-34% depending on income level and location. According to Japan's National Tax Agency, branches must maintain separate books and calculate taxable income as if they were independent corporations. Transfer pricing rules apply to intra-company transactions between the branch and foreign head office, and the NTA scrutinizes branch profit allocations closely. Companies must also decide whether to report under Japanese accounting standards (J-GAAP) or IFRS, a decision that affects financial reporting and consolidation.

Advantages

The primary advantage is simplicity and control. There is no need to establish a separate board of directors or governance structure. The parent company maintains direct control over all operations. Setup costs are the lowest among the three options, and the process takes only 2-3 weeks. For companies performing liaison, market research, or representative functions rather than extensive commercial operations, a branch can be adequate.

Disadvantages

The lack of liability protection is the most significant disadvantage. Some Japanese companies prefer to work with locally incorporated entities, perceiving branches as representing less commitment to the market. Branches may also face limitations: some licenses and permits are only available to Japanese legal entities, and banking relationships can be more difficult to establish.

When a Branch Makes Sense

A branch makes sense for companies in the exploratory phase, conducting market research, or establishing a representative presence before committing to full operations. Companies providing professional services where the parent company's reputation is central to the business sometimes find the branch structure suitable. However, for most businesses planning substantial commercial operations, the liability exposure typically outweighs the cost savings. If you plan to hire local employees, you need to understand Japanese HR compliance requirements regardless of entity type.

Side-by-Side Comparison

The following tables compare all three entity types across formation requirements, ongoing obligations, and operational characteristics to help you evaluate which structure fits your situation.

| Feature | Kabushiki Kaisha (KK) | Goudou Kaisha (GK) | Branch Office |

|---|---|---|---|

| Entity Type | Stock company (corporation) | Limited liability company | Extension of foreign parent |

| Registration Fees | ~¥242,000 | ~¥100,000 | ~¥90,000 |

| Total Setup Cost | ¥300,000 - ¥500,000 | ¥150,000 - ¥300,000 | ¥150,000 - ¥250,000 |

| Setup Timeline | 4-6 weeks | 3-4 weeks | 2-3 weeks |

| Minimum Capital | ¥1 (legal minimum since 2006) | ¥1 (legal minimum since 2006) | None required |

| Liability Protection | Yes - Limited liability | Yes - Limited liability | No - Parent fully liable |

| Governance Requirements | Board of directors, shareholder meetings, potentially auditors | Member-managed, flexible structure | Direct parent control, minimal requirements |

| Market Credibility | Highest - Traditional preference | Growing - Widely accepted | Lower - Seen as less committed |

| Administrative Burden | High | Moderate | Low |

| Ongoing Costs | High | Moderate | Low |

| Ability to Issue Stock | Yes - Can issue shares | No - Membership interests only | No - Not applicable |

| Fundraising Capability | Excellent - VC/IPO ready | Limited - Difficult to raise capital | Very limited |

| Privacy | Director info is public | Member info not public | Representative info public |

| Tax Treatment | Japanese corporate tax on Japan income (~30-34%) | Japanese corporate tax on Japan income (~30-34%) | Japanese tax on Japan income (transfer pricing complexity) |

| Best For | Large operations, traditional partners, seeking investment, long-term commitment | Wholly-owned subsidiaries, SMEs, cost-conscious businesses, modern industries | Market testing, representative functions, liaison activities |

Ongoing Compliance and Tax Comparison

Beyond formation, each structure carries different annual obligations and tax treatment considerations. The following table compares ongoing requirements that affect operating costs and administrative workload.

| Ongoing Requirement | KK | GK | Branch Office |

|---|---|---|---|

| Annual Shareholder / Member Meeting | Required (at least annually) | Not required (member consent sufficient) | Not applicable |

| Auditor Appointment | Required above certain thresholds | Not required | Not applicable |

| Corporate Tax Filing | Required (national + local) | Required (national + local) | Required (national + local) |

| Consumption Tax Registration | Required if revenue exceeds ¥10M | Required if revenue exceeds ¥10M | Required if revenue exceeds ¥10M |

| Transfer Pricing Documentation | Applicable for related-party transactions | Applicable for related-party transactions | Mandatory for all parent-branch transactions |

| Withholding Tax on Profit Repatriation | Dividend withholding (treaty rates apply) | Dividend withholding (treaty rates apply) | No withholding (same legal entity) |

| Annual Registration Renewal | Director re-registration every 2-10 years | No periodic re-registration | Representative changes require re-registration |

| Per-Capita Inhabitants Tax | ¥70,000-¥380,000/year (even at zero profit) | ¥70,000-¥380,000/year (even at zero profit) | ¥70,000-¥380,000/year (even at zero profit) |

| Social Insurance Enrollment | Mandatory from first employee | Mandatory from first employee | Mandatory from first employee |

| Estimated Annual Compliance Cost | ¥1,500,000 - ¥3,000,000+ | ¥800,000 - ¥1,500,000 | ¥600,000 - ¥1,200,000 |

All three structures are subject to Japan's combined corporate tax rate of approximately 30-34% on Japan-sourced income, comprising national corporate tax at 23.2%, prefectural enterprise tax, inhabitants tax, and local corporate tax. According to PwC's Worldwide Tax Summaries, the effective combined rate for standard corporations in Tokyo is approximately 31.5%. Tax treaties between Japan and the parent company's home country can significantly affect withholding rates on dividends (for KK and GK subsidiaries) and branch profit remittances. For detailed information on tax obligations, see our Japan tax filing and compliance guide.

How to Choose the Right Structure

The right entity structure depends on your business model, growth plans, target market, budget, and risk tolerance. No single structure is universally superior.

Decision Framework

Start by evaluating these factors:

Timeline and commitment level: If you are testing the market, a branch office allows entry in 2-3 weeks with the option to convert to a subsidiary later. If you are making a long-term commitment, incorporate from the start to avoid conversion costs.

Liability concerns: If your activities involve significant commercial risk, employee management, or potential for disputes, the limited liability protection of a KK or GK is essential. The branch structure exposes the parent company's global assets.

Target customers and partners: If you are primarily working with traditional Japanese corporations or government entities, a KK provides a credibility advantage. If you are in e-commerce, SaaS, or working with international partners, a GK is typically sufficient.

Capital and growth plans: If you anticipate seeking investment from Japanese VCs or pursuing an IPO, a KK provides the necessary share issuance capability. If you are establishing a wholly-owned subsidiary with no plans for outside investment, a GK offers more flexibility at lower cost.

Budget constraints: If capital is limited, a GK saves approximately ¥150,000-¥200,000 in formation costs compared to a KK, with ongoing compliance savings of ¥500,000-¥1,500,000 annually. For more strategic entity structuring considerations including joint ventures, LLPs, and conversion pathways, see our guide on strategic approaches to entity structuring for Japan entry.

Common Scenarios

Large multinational establishing a significant Japanese subsidiary: Kabushiki Kaisha. The higher costs are justified by credibility requirements, and the company has the resources to manage compliance.

Technology startup or e-commerce company entering Japan: Goudou Kaisha. Lower costs and simpler administration are ideal for growing companies, and credibility concerns are minimal in these industries.

Manufacturing company establishing a production facility: Kabushiki Kaisha. Liability exposure and the need to work with traditional Japanese suppliers and partners favor the KK structure.

Professional services firm providing consulting or advisory services: Goudou Kaisha or branch office, depending on liability concerns and client relationship requirements.

Foreign company testing the Japanese market before full commitment: Branch office initially, with plans to convert to a GK or KK if the market test is successful.

Wholly-owned subsidiary with no plans for external investment: Goudou Kaisha. The parent company's investment is sufficient, and the operational flexibility and cost savings are valuable. Similarly, choosing the right corporate bank for your entity type can streamline operations and reduce administrative burden.

Working with Professionals

Regardless of which structure you choose, working with qualified legal and tax advisors is essential. Japanese corporate law and tax regulations are complex, and the consequences of missteps can be costly. Engage advisors with experience in Japanese corporate structures and cross-border operations who understand how your entity choice interacts with your home country's tax system. Be wary of choosing a structure based solely on cost: the difference between a GK and KK might save ¥200,000 in formation costs, but if that choice costs a major contract or creates ongoing operational challenges, it is a poor economy.

Frequently Asked Questions

Can a foreign company convert a GK to a KK later?

Yes. Japan's Companies Act permits conversion from a GK to a KK (and vice versa). The process involves amending the articles of incorporation, filing with the Legal Affairs Bureau, and paying additional registration fees. Conversion typically takes 4-6 weeks and costs approximately ¥300,000-¥500,000 in registration and professional fees. Many foreign companies start with a GK to minimize initial costs and convert to a KK when business growth or fundraising needs require the stock company structure.

Do I need a Japanese resident to serve as director or representative?

For a KK or GK, there is no legal requirement for a director or member to be a Japanese resident. However, a branch office must appoint a representative in Japan who is authorized to act on behalf of the parent company. In practice, having at least one Japan-based representative is strongly recommended for all entity types, as it simplifies bank account opening, government filings, and day-to-day operations. Some banks require a Japan-resident signatory to open a corporate account.

What is the effective corporate tax rate for each entity type?

All three structures face the same corporate tax rates on Japan-sourced income. The combined effective rate (national corporate tax, enterprise tax, inhabitants tax, and local corporate tax) ranges from approximately 30% to 34% depending on income level and office location. According to PwC's Worldwide Tax Summaries, the standard effective rate in Tokyo is approximately 31.5%. SMEs with capital of ¥100 million or less qualify for a reduced 15% national rate on the first ¥8 million of taxable income. For comprehensive tax rate details, see our corporate income tax guide.

How much capital should I actually set aside for a KK or GK?

While the legal minimum capital is ¥1 for both KK and GK, practical requirements are higher. Most Japanese banks require demonstrable capitalization to open a corporate account, with ¥5 million to ¥10 million being a common threshold for foreign-owned entities. Capital below ¥5 million may also raise concerns with potential business partners about the company's financial stability. The appropriate capital level depends on your planned activities, visa requirements for foreign employees, and the expectations of your industry sector.

Can a branch office hire employees in Japan?

Yes. A branch office can hire employees in Japan and must comply with the same labor laws, social insurance obligations, and tax withholding requirements as a KK or GK. The branch must register with the labor standards inspection office, enroll in social insurance programs, and withhold income tax from employee salaries. However, some prospective employees may prefer to work for a locally incorporated entity (KK or GK) rather than a foreign branch, particularly in competitive hiring markets.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.