Japanese Corporate Banks Compared: How to Decide on Which Corporate Bank to Apply to

Key Takeaways

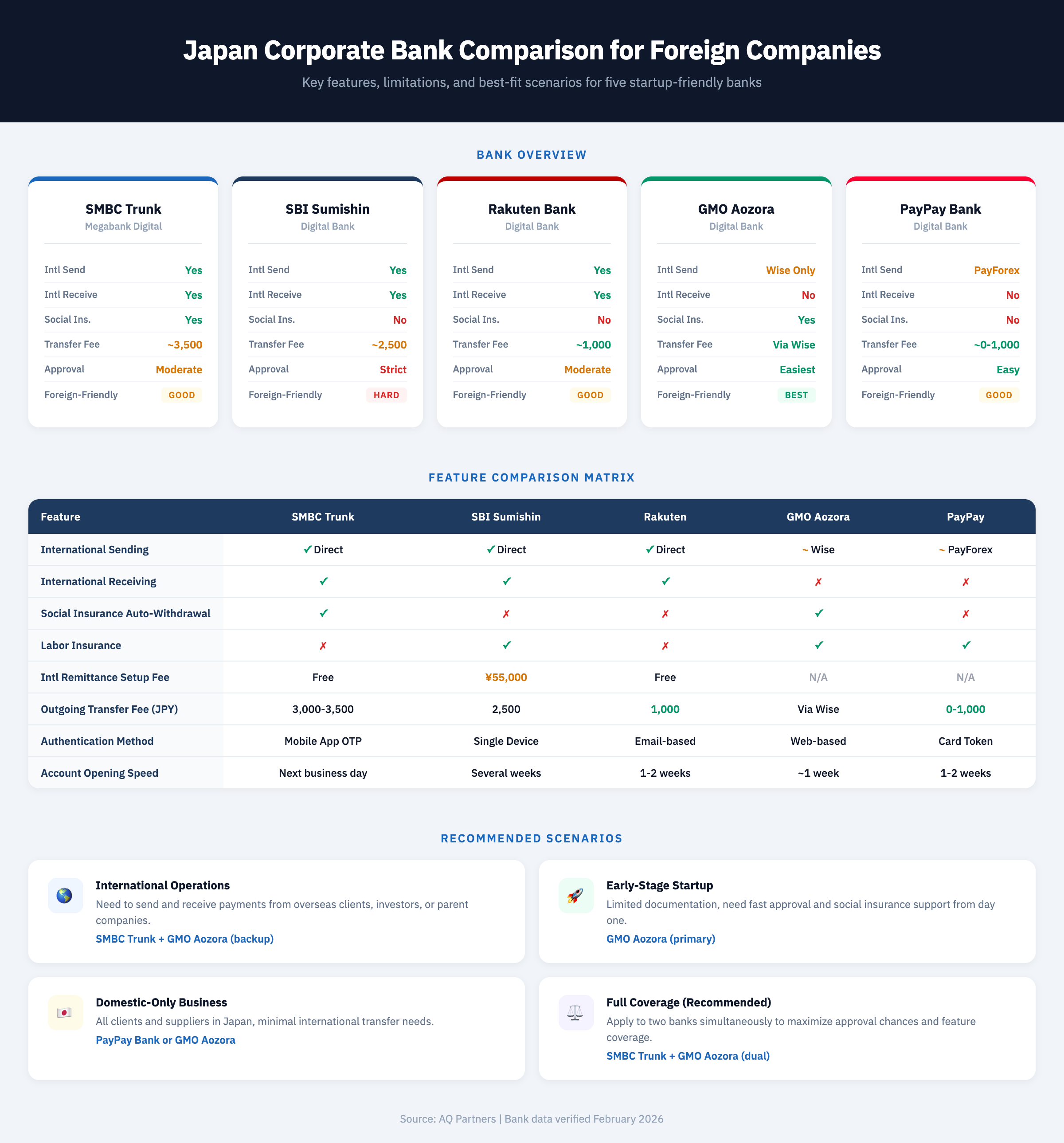

- Japan's three megabanks (MUFG, SMBC, Mizuho) serve only about 19.3% of all Japanese companies as primary banks — their rigorous screening makes them difficult for newly incorporated foreign companies, but SMBC Trunk now offers a startup-friendly digital pathway with next-business-day account activation.

- International remittance capability is the single biggest differentiator between banks — only SMBC Trunk, SBI Sumishin Net Bank, and Rakuten Bank support both sending and receiving foreign payments. GMO Aozora and PayPay Bank are limited to outgoing transfers through third-party integrations.

- Social insurance automatic withdrawal support eliminates a critical monthly compliance burden — only SMBC Trunk and GMO Aozora Net Bank offer this feature among the banks compared, making them essential for companies with employees in Japan.

- Transfer fees range from nearly free to JPY 3,500 per transaction — Rakuten Bank offers the lowest direct outgoing rate at JPY 1,000, while PayPay Bank can achieve near-zero costs through PayForex. SBI Sumishin charges a JPY 55,000 international remittance setup fee.

- Applying to SMBC Trunk and GMO Aozora Net Bank simultaneously is the optimal strategy — this combination maximizes approval probability while covering both international operations and domestic compliance needs, and is recommended by most Japan market-entry advisors.

Key Factors to Consider When Choosing a Corporate Bank

Choosing a corporate bank in Japan involves evaluating international remittance capabilities, social insurance automation, approval accessibility, and authentication infrastructure. The right combination depends on your business model, whether you receive overseas payments, and how quickly you need an operational account.

Choosing the right corporate bank in Japan can feel like navigating a maze. Unlike in many Western countries where business banking is relatively straightforward, Japan's corporate banking landscape requires careful consideration of factors that go far beyond interest rates and monthly fees. The bank you choose will impact everything from your ability to receive payments from international clients to whether you can automate your social insurance payments.

For startups and foreign companies establishing operations in Japan, this decision becomes even more critical. Opening a corporate bank account is often one of the first major hurdles you'll face, and the wrong choice can lead to operational headaches, rejected international transfers, or the need to open multiple accounts to cover basic business needs. For a detailed walkthrough, see our complete guide to opening a corporate bank account in Japan.

Japan's banking landscape splits into two main categories: traditional mega-banks like SMBC, which offer stability and credibility but often come with more bureaucratic processes, and digital-first banks like GMO Aozora Net Bank and PayPay Bank, which provide flexibility and ease of use but may lack certain features. Then there are hybrid options that attempt to bridge both worlds. According to the Japan Bankers Association, there are currently over 100 member banks including city banks, regional banks, and trust banks — though only a handful are practical options for newly incorporated foreign companies.

In this guide, we'll compare five of the most popular corporate banking options for businesses in Japan: SMBC Trunk, SBI Sumishin Net Bank, Rakuten Bank, GMO Aozora Net Bank, and PayPay Bank. We'll break down the key factors you need to consider, from international remittance capabilities to application requirements, and help you determine which bank (or combination of banks) makes the most sense for your business needs. By the end, you'll have a clear framework for making this crucial decision and setting up your back-office operations and financial systems in Japan.

Why Megabanks Are Hard for Newly Incorporated Businesses

Japan's traditional megabanks (Mitsubishi UFJ, Sumitomo Mitsui (SMBC), and Mizuho) offer unparalleled credibility and comprehensive services. A Tokyo Shoko Research survey of over 1.6 million companies found that these three megabanks collectively serve approximately 19.3% of all surveyed companies as primary banks — with MUFG leading at 7.93% (127,264 companies), SMBC at 6.34% (101,697 companies), and Mizuho at 5.04% (80,840 companies). However, opening a corporate account at these institutions as a newly incorporated company (regardless of whether you chose KK, GK, or branch office structure), especially a foreign-founded one, can be extremely difficult. These banks typically require extensive business track records, detailed financial projections, proof of existing contracts or revenue, and in many cases, personal introductions or referrals from existing corporate clients.

The screening process at megabanks is notoriously rigorous and slow, often taking several weeks or even months. They're primarily designed to serve established corporations with proven business models and substantial capital. For a startup that just completed incorporation and post-incorporation filings and has minimal documentation, a business plan that's still evolving, or founders without extensive networks in Japan, getting approved for a standard megabank account is often unrealistic.

This reality has given rise to startup-friendly alternatives. SMBC Trunk, for instance, is SMBC's answer to this problem — a product specifically designed to make megabank services accessible to newly established companies while maintaining the credibility of the SMBC name. Launched in May 2025, SMBC Trunk targets Japan's approximately 3.36 million SMEs and has set an ambitious goal of acquiring 300,000 accounts within three years. Similarly, digital banks like GMO Aozora Net Bank and Rakuten Bank have positioned themselves as more accessible options, with streamlined application processes and more flexible documentation requirements that recognize the realities of early-stage companies.

International Remittance Capabilities

If your business receives payments from overseas clients or pays foreign contractors, international remittance capabilities should be your top priority. Not all Japanese corporate banks offer this feature, and among those that do, the implementation varies dramatically.

Full international remittance support — offered by SMBC Trunk, SBI Sumishin Net Bank, and Rakuten Bank — allows you to both send and receive payments in major foreign currencies. However, this isn't automatic. Each bank requires a separate application after your account is opened, with additional screening that includes detailed questions about your business model, transaction volumes, and counterparties. Even if your corporate account is approved, your international remittance application can still be rejected.

The costs add up quickly. Expect transfer fees ranging from JPY 1,000 to JPY 3,500, correspondent bank fees of JPY 1,000 to JPY 2,500, and additional lifting charges. SBI Sumishin Net Bank also requires proof of remittance (invoices, contracts) for every incoming transfer, adding administrative burden.

Some banks offer limited solutions through third-party services. GMO Aozora Net Bank integrates with Wise for outgoing transfers only, while PayPay Bank uses PayForex for the same. These options are cheaper and easier to set up, but you cannot receive international payments through these accounts — a dealbreaker for many businesses.

For companies with significant international operations, this feature alone often determines which bank becomes your primary account.

Social Insurance Automatic Withdrawal

Social insurance automatic withdrawal is a make-or-break feature for companies hiring employees and securing work visas in Japan. Every month, businesses must handle HR compliance requirements including social insurance premiums for their staff, and manual payments create unnecessary administrative work and risk of missed deadlines.

Only three banks in this comparison support automatic withdrawal: SMBC Trunk, GMO Aozora Net Bank, and PayPay Bank. SBI Sumishin Net Bank and Rakuten Bank do not offer this feature, meaning you'll need to manually process these payments each month or maintain a separate account at a bank that does support it.

For lean startups and small teams, this limitation can be a significant operational burden. Many companies solve this by using a bank without social insurance support as their main operating account, while maintaining a secondary account at GMO Aozora Net Bank or another compatible bank specifically for payroll and social insurance. However, this means managing multiple accounts and ensuring sufficient funds are transferred between them each month — an added layer of complexity that's entirely avoidable by choosing the right primary bank from the start.

Authentication and Digital Infrastructure

How you access and secure your corporate account matters more than you might think, especially for remote teams or founders splitting time between countries. Each bank takes a different approach to authentication, with varying implications for usability and security.

SMBC Trunk uses a mobile app-based one-time password system, but there's a catch: you need access to the Japanese App Store to download it. This can be problematic for foreign founders who haven't yet obtained Japanese phone numbers or set up Japanese Apple IDs.

SBI Sumishin Net Bank offers authentication via mobile or PC, but with a significant limitation — you can only link one device (typically a smartphone) to the account. If you lose that device or need to switch phones, you'll need to go through a re-registration process. This single-device restriction can be frustrating for businesses that need multiple people to access the account or founders who regularly switch between devices.

Rakuten Bank uses email-based remittance authentication, which is straightforward and accessible from any device. PayPay Bank employs card-based token authentication, requiring you to have the physical card on hand for certain transactions.

GMO Aozora Net Bank provides the most flexibility with standard web-based electronic banking that doesn't impose unusual device restrictions. They also issue a debit card immediately upon account opening, which can be useful for business expenses before your corporate credit card arrives.

For distributed teams or international founders, these authentication differences can significantly impact daily operations. Choose a system that matches how your team actually works.

Bank-by-Bank Breakdown

Each of the five banks compared here occupies a distinct niche — from megabank credibility to startup-first simplicity. The breakdown below covers strengths, limitations, and ideal use cases for each option.

Now that we've covered the critical factors to consider, let's examine each bank in detail. Understanding the specific strengths, limitations, and ideal use cases for each option will help you identify which aligns best with your business needs.

| Category | Item | SMBC Trunk | SBI Sumishin | Rakuten | GMO Aozora | PayPay |

|---|---|---|---|---|---|---|

| International Remittance |

Sending | ✓ | ✓ | ✓ | ✓ | ✓ |

| Receiving | ✓ | ✓ | ✓ | ✗ | ✗ | |

| Separate Application Required | Yes | Yes | Yes | N/A | No | |

| Setup Fee | None | ¥55,000 | None | None | None | |

| Taxes & Insurance |

Social Insurance Auto-Withdrawal | ✓ | ✗ | ✗ | ✓ | ✗ |

| Labor Insurance | ✗ | ✓ | ✗ | ✓ | ✓ | |

| Resident Tax Payment | ✓ | ✓ | ✓ | ✓ | ✓ |

Scroll horizontally to view all banks on mobile devices

SMBC Trunk: The Mega-Bank Option for Credibility

SMBC Trunk is Sumitomo Mitsui Banking Corporation's strategic answer to the startup banking problem. It delivers the credibility and stability of one of Japan's three major megabanks while removing many of the barriers that make traditional megabank accounts inaccessible to newly incorporated companies. Launched in May 2025, SMBC Trunk enables next-business-day account opening via smartphone — the first time a Japanese megabank has offered this speed for corporate accounts.

Best for: Companies that need the legitimacy of a major bank for client relationships, investor confidence, or partnerships with established Japanese corporations. If you're raising venture capital or working with large enterprises that prefer dealing with recognized financial institutions, SMBC Trunk provides that seal of approval.

Strengths: Full international remittance capabilities for both sending and receiving payments, social insurance automatic withdrawal support, and the backing of a tier-one financial institution. The account comes with comprehensive digital banking features through a mobile app, making day-to-day operations smooth once you're set up.

Limitations: International remittance requires a separate application through their Global e-Trade service, which involves detailed screening including phone interviews. Even if your SMBC Trunk account is approved, the international remittance application can be rejected. The fees are also on the higher end (JPY 3,000–3,500 per transfer + correspondent bank fees of JPY 2,500 and lifting charges). You'll need access to the Japanese App Store for the authentication app, which can be inconvenient for international founders.

SMBC Trunk works best as a primary operating account for companies that value institutional credibility and need comprehensive banking services, provided you can navigate the application requirements and accept the premium pricing structure.

SBI Sumishin Net Bank: The Tech-Forward Choice

SBI Sumishin Net Bank is a major online bank that has built a strong reputation among technology-focused companies and digital-native startups in Japan. It combines low domestic transfer fees with robust digital operations, but demands more from applicants than most other options.

Best for: Established startups with solid documentation, clear business models, and the administrative capacity to handle detailed screening processes. If you have existing contracts, a well-developed business plan, and can articulate your operations clearly, SBI Sumishin Net Bank offers excellent value.

Strengths: Full international remittance capabilities with competitive transfer fees starting at JPY 2,500. The digital platform is sophisticated and reliable, designed for companies that operate primarily online. Once approved, the account provides strong functionality for tech companies that prioritize efficient digital banking infrastructure.

Limitations: This is arguably the most difficult account to open among the digital banks. SBI Sumishin Net Bank frequently requests extensive additional documentation after the initial application, and the screening process is thorough. International remittance requires a separate JPY 55,000 setup fee — significantly higher than competitors. You must provide proof of remittance (invoices, contracts) for every incoming transfer, creating ongoing administrative overhead. The account only links to one device, which can be restrictive. Most critically, it does not support social insurance automatic withdrawal, forcing you to maintain a separate account or handle these payments manually.

SBI Sumishin Net Bank makes sense for companies with strong documentation and primarily domestic operations who value low transfer fees and digital efficiency, but can live without social insurance automation. The high international remittance setup fee makes it less attractive for companies with frequent cross-border transactions.

Rakuten Bank: The Accessible Digital Bank

Rakuten Bank is one of Japan's largest digital banks, leveraging the Rakuten ecosystem's reach to offer straightforward business banking for small and medium-sized companies. It strikes a balance between accessibility and functionality, making it a popular choice for companies prioritizing ease of use.

Best for: Companies wanting seamless integration with online services and e-commerce platforms, particularly those already using other Rakuten business tools. It's well-suited for businesses focused on digital operations with moderate international payment needs.

Strengths: International remittance is supported with the most competitive transfer fees in this comparison — just JPY 1,000 for outgoing transfers. Receiving international payments requires no separate application, simplifying the setup process. The email-based authentication system is straightforward and accessible from any device. The platform integrates smoothly with various online business services, reflecting Rakuten's broader digital ecosystem.

Limitations: No social insurance automatic withdrawal support, which means manual monthly payments or maintaining a secondary account. You must have a 03 fixed-line phone number to open the account — a hurdle for startups using only mobile phones or virtual offices. While receiving international payments is easy, sending money still requires a separate application. Incoming remittance fees are JPY 2,000 per transfer, which adds up for companies with frequent international receipts.

Rakuten Bank works well as a primary account for digitally-focused businesses with regular international income who can manage social insurance payments separately. The low outgoing transfer fees make it particularly attractive for companies that frequently pay overseas contractors or suppliers, but the 03 phone number requirement can be a dealbreaker for some startups.

GMO Aozora Net Bank: The Flexible Startup Favorite

GMO Aozora Net Bank has become the go-to choice for startups and small businesses in Japan, earning its reputation through pragmatic onboarding and an understanding of what early-stage companies actually need. It's frequently recommended in startup circles precisely because it removes many of the friction points found at other banks.

Best for: Newly incorporated startups with limited documentation, companies needing quick account setup, and businesses that want to use a digital bank alongside a megabank for operational efficiency. It's the most startup-friendly option in this comparison.

Strengths: The most accessible application process with flexible documentation standards that acknowledge the realities of early-stage companies. Social insurance automatic withdrawal is fully supported, eliminating a major administrative burden. You receive a debit card immediately upon opening the account, useful for business expenses before other payment methods are established. The digital banking platform is straightforward without unnecessary device restrictions. The approval process is typically faster than competitors.

Limitations: International remittance is severely limited — you can only send money through Wise integration, and you cannot receive international payments at all. This is the critical dealbreaker for businesses with overseas clients. There's no direct pathway to full international banking services, so if your business model depends on receiving foreign payments, GMO Aozora Net Bank cannot be your only account.

GMO Aozora Net Bank excels as either a primary account for purely domestic businesses or as a secondary account paired with a bank that handles international remittances. Many companies use it specifically for payroll and social insurance while maintaining SMBC Trunk or Rakuten Bank for international transactions. The combination strategy is common and effective, though it adds account management complexity.

PayPay Bank: The Simple Domestic Solution

PayPay Bank is designed for straightforward, low-cost domestic business banking with minimal complexity. It strips away advanced features to focus on what small operations conducting business primarily within Japan actually need on a daily basis.

Best for: Small businesses, freelancers, and companies with purely domestic operations who want simple banking without international complications. If your clients, suppliers, and contractors are all in Japan, PayPay Bank delivers efficiency at the lowest cost.

Strengths: The simplest fee structure with outgoing international transfers costing approximately JPY 0–1,000 through PayForex integration — dramatically cheaper than competitors. No correspondent bank fees, making the costs predictable. Card-based token authentication provides solid security. Transfer data is handled in English, which can be helpful for international founders navigating Japanese banking systems.

Limitations: Like GMO Aozora Net Bank, international remittance is severely restricted — you can only send money through PayForex, and you cannot receive international payments. This eliminates it as an option for any business that needs to invoice overseas clients. Social insurance automatic withdrawal is not supported, which limits its utility for companies with employees.

PayPay Bank makes sense for businesses with exclusively domestic revenue streams who occasionally need to make international payments to suppliers or service providers. The ultra-low transfer fees are genuinely attractive, but the inability to receive foreign payments makes it unsuitable as a sole banking solution for internationally-oriented companies. It works best as a secondary account for specific use cases or as the primary account for businesses firmly committed to the Japanese market only.

AQ Partners Suggestion: Applying to Multiple Banks

The most effective strategy is applying to two banks simultaneously — SMBC Trunk for megabank credibility and international capability, plus GMO Aozora Net Bank for startup-friendly approval and domestic compliance coverage.

Full Coverage with Multiple Banks

Our recommendation is straightforward: apply to both SMBC Trunk and GMO Aozora Net Bank simultaneously. This combination gives you the best chance of success while covering all essential banking functions if both applications are approved.

SMBC Trunk provides the megabank credibility, full international remittance capabilities (both sending and receiving), and social insurance automatic withdrawal. It positions your company professionally with clients, investors, and partners who value institutional legitimacy.

GMO Aozora Net Bank offers the most accessible approval process, immediate debit card issuance, social insurance support as a backup, and flexible digital banking. If SMBC Trunk's international remittance application gets rejected or delayed, you still have basic outgoing transfer capabilities through GMO's Wise integration.

By applying to both simultaneously, you maximize your chances of getting at least one account approved quickly. If both succeed, you have an ideal setup: SMBC Trunk as your primary operating account for international business and client interactions, with GMO Aozora Net Bank serving as your domestic operations and payroll account. If only one approves, you can function immediately and apply for the other later once your business has more transaction history.

No Guarantees of a Successful Application

Even with perfect documentation and a solid business plan, bank account approval in Japan is never guaranteed. Each bank conducts independent screening based on criteria that aren't fully transparent, and decisions can seem arbitrary or inconsistent.

Factors beyond your control can influence outcomes: your industry, your business model's perceived risk, the bank's current regulatory environment, or even how well you articulate your plans during phone interviews. Foreign-founded companies often face additional scrutiny, regardless of how legitimate the business is. The JETRO banking and finance guide outlines required documentation including registry certificates, company seal certificates, representative identification, business plans, and sometimes office lease evidence — but meeting all requirements still does not guarantee approval.

This uncertainty is exactly why applying to multiple banks makes sense. Don't put all your eggs in one basket and risk weeks of delay if that single application fails. The time invested in preparing applications for two banks simultaneously is minimal compared to the cost of having no corporate account while you sequentially try different options. Start the process early, apply broadly, and be prepared to work with whichever combination of banks approves your applications.

Conclusion

Choosing a corporate bank in Japan requires balancing international capabilities, approval accessibility, and operational features like social insurance automation. There's no perfect solution for every business — your ideal setup depends on whether you need to receive foreign payments, how much documentation you can provide, and whether megabank credibility matters for your clients and investors.

For most foreign companies, we recommend applying to both SMBC Trunk and GMO Aozora Net Bank simultaneously. This maximizes your approval chances while covering essential banking functions if both succeed. Japan's banking system — overseen by the Bank of Japan and regulated under the Banking Act — is stable and well-capitalized, so whichever combination you choose, your deposits and operations are protected. Start your applications early, prepare thorough documentation, and don't be discouraged by rejections — many successful companies went through multiple attempts before finding the right banking setup. Your initial choice isn't permanent; you can always add accounts or switch as your business grows and needs evolve.

For guidance on preparing your corporate inkan (corporate seal) and other documentation required for bank applications, or for help navigating your entity structuring strategy for Japan market entry, AQ Partners provides hands-on support through the entire process.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.