Complete Guide To Opening a Corporate Bank Account in Japan

Key Takeaways

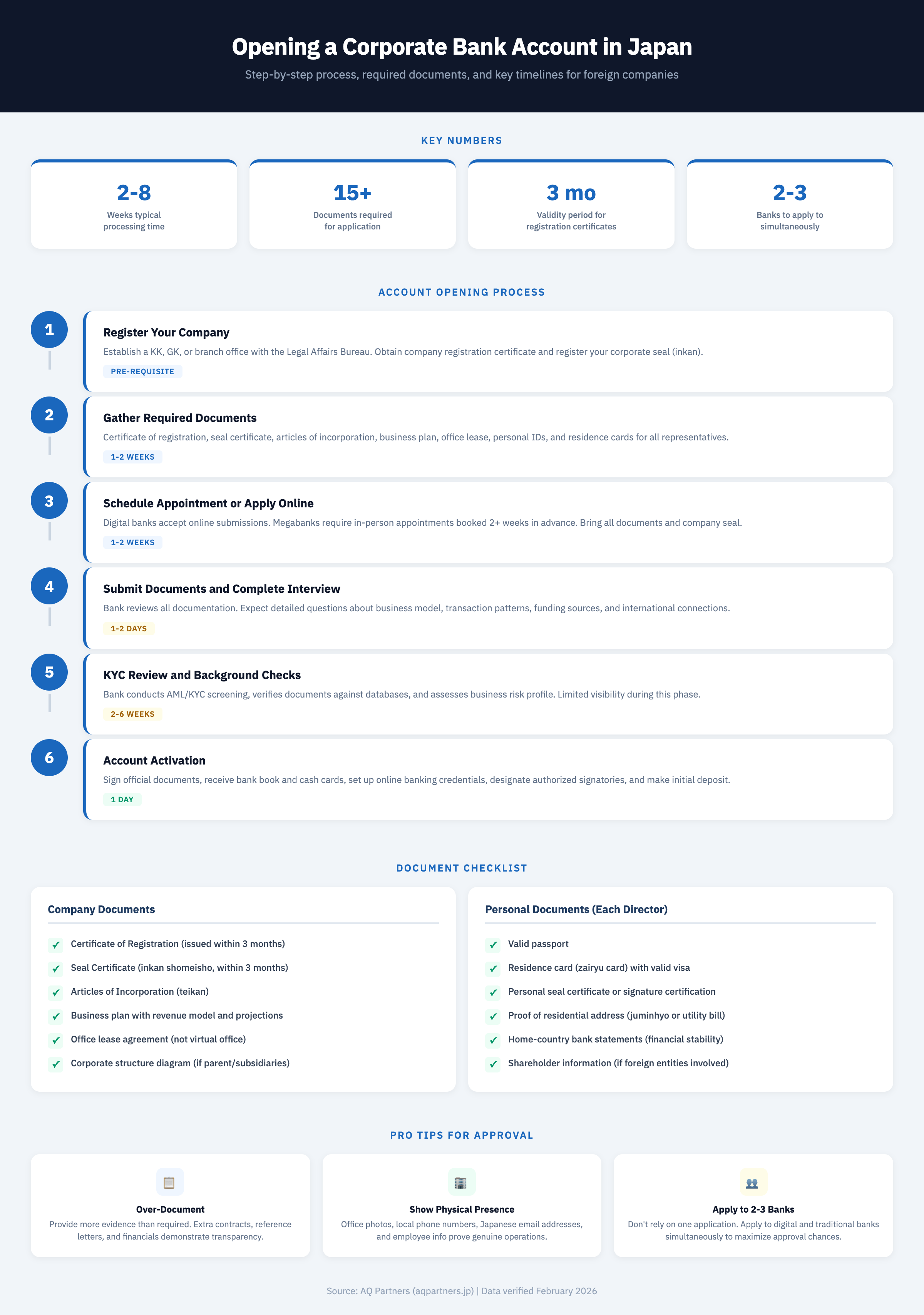

- Japan's corporate bank account opening process takes 2-8 weeks on average -- digital banks like GMO Aozora Net Bank can approve applications in as little as one week, while megabank applications at MUFG, SMBC, or Mizuho routinely take 4-8 weeks due to rigorous KYC screening.

- Registration certificates and seal certificates must be issued within three months of your application date -- expired documents are the single most common reason for application delays, so time your Legal Affairs Bureau requests carefully around your bank appointment schedule.

- Applying to 2-3 banks simultaneously is the recommended strategy -- according to JETRO, the required documentation is largely the same across institutions, meaning the marginal effort of parallel applications is low while the risk reduction is significant.

- A physical office address is a non-negotiable requirement at virtually all banks -- virtual offices and mail forwarding services are rejected by most institutions, and co-working spaces require proof of a dedicated desk or private office rather than shared-access membership.

- Foreign-owned companies face additional scrutiny but have viable pathways -- Japan's Financial Services Agency oversees banking regulations that require strict AML/KYC compliance, yet startup-friendly digital banks and SMBC Trunk have specifically designed onboarding processes for newly incorporated foreign entities.

Prerequisites: What You Need Before Applying

Before applying to any Japanese bank, you need a registered entity, a full set of corporate and personal documents issued within validity windows, and proof of genuine business operations in Japan -- missing even one item can delay or derail the process.

Opening a corporate bank account in Japan is one of the first major hurdles foreign entrepreneurs and businesses face when establishing operations in the country. Unlike many Western countries where business banking is relatively straightforward, Japan's corporate banking landscape requires careful navigation, extensive documentation, and significant patience. The Financial Services Agency (FSA), which oversees all banking institutions in Japan, enforces strict Anti-Money Laundering (AML) and Know Your Customer (KYC) standards that banks must comply with during every account opening. However, with the right preparation and understanding of the process, you can successfully open an account that supports your business operations and sets the foundation for long-term success in the Japanese market.

This comprehensive guide walks you through everything you need to know about opening a corporate bank account in Japan, from understanding the prerequisites to managing common challenges and making the most of your banking relationship once your account is approved.

Company Registration Requirements

First and foremost, you must have a registered Japanese entity. This typically means establishing a Kabushiki Kaisha (KK, equivalent to a corporation), a Godo Kaisha (GK, similar to an LLC), or registering a branch office of your foreign company. You cannot open a corporate bank account before your company is officially registered with the Legal Affairs Bureau. According to the Japan Bankers Association (JBA), Japan has over 100 member banks including city banks, regional banks, and trust banks -- but all share these baseline registration requirements.

Once registered, you'll need a Certificate of Registration (登記事項証明書, tokki jiko shomeisho), which is the official document proving your company's legal existence in Japan. Banks typically require a copy issued within the last three months, so timing matters. If your certificate is older than this, you'll need to obtain a fresh copy from the Legal Affairs Bureau before applying.

Your company seal (会社実印, kaisha jitsuin) is equally critical. In Japan, corporate seals carry the same legal weight as signatures in Western countries, and banks require both the physical seal and a seal certificate (印鑑証明書, inkan shomeisho) from the Legal Affairs Bureau. This certificate verifies that your company seal is officially registered and authentic. Like the registration certificate, seal certificates are typically only valid for three months for banking purposes.

Business Documentation

Banks want to understand what your company actually does and whether it represents a legitimate business operation. This means preparing comprehensive business documentation that clearly articulates your business model, revenue streams, and operational structure.

Your Articles of Incorporation should outline your company's purpose, structure, and governance. While banks receive a version of this through your registration certificate, having the complete document available demonstrates preparedness and professionalism.

A detailed business plan or business overview is essential, particularly for newly incorporated companies without operational history. This document should explain your products or services, target market, competitive landscape, revenue model, and financial projections. For foreign-founded companies, banks are especially interested in understanding why you've chosen to operate in Japan and how you plan to conduct business in the local market.

Proof of a physical office address is mandatory. A virtual office or mail forwarding service is generally not acceptable for opening a corporate bank account. You'll need to provide an office lease agreement showing your company name as the tenant. If you're using a co-working space, you'll need documentation proving you have a dedicated address, not just access to shared facilities.

Personal Requirements for Representatives

Japanese banks don't just vet your company. They also thoroughly examine the individuals behind it, particularly directors and authorized signatories.

Every director and authorized representative must provide a valid passport and, if residing in Japan, a residence card (在留カード, zairyu card). The residence card proves legal residency status, and banks pay close attention to visa categories and expiration dates. Certain visa types, particularly tourist visas or short-term business visas, may raise red flags or result in automatic rejection.

A personal seal certificate (印鑑証明書, inkan shomeisho) for each representative is also required. Foreign nationals who haven't registered a personal seal can sometimes use signature certification instead, but this varies by bank and should be confirmed beforehand.

Proof of your residential address in Japan (typically a utility bill, residence certificate (住民票, juminhyo), or lease agreement) rounds out the personal documentation requirements. Banks want to verify that representatives have genuine connections to Japan and aren't simply visiting temporarily.

Step-by-Step Application Process

The corporate account application process follows six stages -- from scheduling an appointment through to account activation -- with the KYC review period of 2-6 weeks representing the longest and least transparent phase.

With all prerequisites satisfied, you're ready to begin the formal application process. Understanding what happens at each stage helps set realistic expectations and reduces anxiety during what can be a lengthy and opaque process. The process does change based on the bank you are applying for. For example, certain banks offer a fully online application process. You can learn more about which corporate bank account is best for you in this article, Japanese Corporate Banks Compared: How to Decide on Which Corporate Bank to Apply To.

Initial Consultation and Appointment

The application process varies significantly depending on the type of bank you choose. Many digital banks now offer completely online application processes, allowing you to submit documents electronically before ever speaking with a bank representative. SMBC Trunk, GMO Aozora Net Bank, PayPay Bank, and Rakuten Bank, for example, let you upload all required documentation through their websites and only require in-person visits for final account activation or specific circumstances.

Traditional banks and megabanks, however, typically still require you to schedule an appointment before submitting a corporate account application. Walk-in applications are rarely accepted, particularly at major institutions like MUFG, SMBC, and Mizuho. Contact your chosen bank's corporate banking department at least two weeks in advance, as popular banks may have limited appointment slots.

Hybrid approaches are becoming more common, where you submit initial documentation online or via email, then attend an appointment only after preliminary screening. SMBC Trunk, for instance, allows online pre-application before scheduling formal meetings.

The following table provides a high-level comparison of the main types of banks available in Japan for corporate accounts, which can help you decide where to apply:

| Feature | Megabanks (MUFG, SMBC, Mizuho) | Regional Banks (Yokohama Bank, Chiba Bank, etc.) | Online Banks (GMO Aozora, PayPay, Rakuten) |

|---|---|---|---|

| English Support | Limited; select branches with international desks | Rare; almost exclusively Japanese | Moderate to good; GMO Aozora offers English interface |

| Online Banking | Full-featured but interface is often Japanese-only | Available but typically basic and Japanese-only | Fully online with modern UI; some offer English |

| Application Process | In-person appointment required; extensive documentation | In-person at local branch; relationship-driven | Fully online submission; minimal in-person steps |

| Approval Difficulty for Foreign Companies | High; strict KYC and conservative risk assessment | Moderate; may prefer locally operating businesses | Lower; designed to be startup-friendly |

| Typical Processing Time | 4-8 weeks | 3-6 weeks | 2-4 weeks |

| Branch Network | Nationwide with extensive ATM coverage | Concentrated in home prefecture and surrounding areas | No physical branches; rely on convenience store ATMs |

| International Wire Transfers | Full support with correspondent bank networks | Available but options may be limited | Varies; some offer competitive rates, others limited |

| Monthly Maintenance Fees | ¥2,000-¥3,000+ | ¥1,000-¥2,500 | Often free for basic accounts |

| Best Suited For | Established businesses needing full-service banking and credibility | Businesses with strong local presence in a specific region | Startups and foreign-owned companies needing quick setup |

If an in-person appointment is required, prepare to bring every document mentioned in the prerequisites section to your first meeting, plus any additional materials the bank specifically requests. Also bring your company seal and, if applicable, your personal seal. Some banks conduct preliminary document reviews during the first appointment, while others simply collect materials for later evaluation.

Document Submission

The document submission phase is where many applications encounter their first hurdles. Japanese banks are meticulous about documentation, and even minor discrepancies can cause problems.

Beyond the core documents already discussed, be prepared to provide:

- Detailed information about your expected monthly transaction volumes, both incoming and outgoing

- Information about your anticipated business partners, clients, and suppliers

- Explanation of your business operations in Japanese (or professional translations)

- Corporate structure diagrams if you have parent companies or subsidiaries

- Shareholder information, particularly if foreign individuals or entities are involved

- Bank statements from your home country showing business or personal financial stability

The JETRO banking and finance guide confirms that required documentation includes registry certificates, company seal certificates, representative identification, business plans, and sometimes office lease evidence. Documents have specific validity periods -- registration certificates and seal certificates are generally only considered current if issued within the past three months. If your application process extends beyond this timeframe, you may need to obtain fresh copies.

The following table summarizes the document requirements across different bank categories, helping you prepare the right materials regardless of which institution you target:

| Document | Megabanks | Regional Banks | Online/Digital Banks | Notes |

|---|---|---|---|---|

| Certificate of Registration (登記事項証明書) | Required (original, within 3 months) | Required (original, within 3 months) | Required (copy or upload accepted) | Must match current company details exactly |

| Corporate Seal Certificate (印鑑証明書) | Required (original, within 3 months) | Required (original, within 3 months) | Required (upload or mail) | Physical seal needed at in-person appointments |

| Articles of Incorporation (定款) | Required (full notarized copy) | Required | Required (scanned copy accepted) | Business purpose must match stated activities |

| Business Plan / Company Overview | Detailed plan with financials required | Business overview required | Basic overview usually sufficient | Include revenue model, target market, projections |

| Office Lease Agreement | Required (must show company name as tenant) | Required | Often required; some accept co-working proof | Virtual offices generally rejected |

| Representative Passport + Residence Card | Required for all directors | Required for representative director | Required (photo upload) | Visa category and expiration dates scrutinized |

| Personal Seal Certificate / Signature Cert. | Required for each signatory | Required for representative | Varies; some accept signature certification | Foreign nationals may use signature notarization |

| Proof of Residential Address (住民票) | Required (within 3 months) | Required | Required (upload) | Utility bill or juminhyo accepted |

| Shareholder / Corporate Structure Info | Required if foreign entities involved | Required for complex structures | May be requested during screening | Include UBO (ultimate beneficial owner) details |

| Home-Country Bank Statements | Frequently requested | Sometimes requested | Rarely requested | Demonstrates financial stability of founders |

Interview Process

After submitting your documents, most banks conduct one or more interviews with company representatives. This isn't a formality -- it's a critical evaluation stage where banks assess the legitimacy of your business and your understanding of Japanese banking regulations.

Banks typically ask detailed questions about:

- Business operations: What exactly does your company do? How do you generate revenue? Who are your customers?

- Transaction patterns: How much money do you expect to flow through the account monthly? What percentage will be domestic versus international? Will transactions be primarily B2B or B2C?

- International connections: If you're receiving or sending international payments, banks want to know the countries involved, the nature of these transactions, and how they relate to your business model.

- Funding sources: Where is your startup capital coming from? If you have investors, who are they and where are they located?

- Purpose of account: Why this specific bank? What banking services do you need immediately versus in the future?

Be honest and thorough in your responses. Inconsistencies between your written documentation and interview answers raise immediate red flags. If you don't speak Japanese fluently, bringing a professional interpreter is advisable. While some banks offer English-language interviews, having your own interpreter ensures nothing is lost in translation.

Review Period

Once documents are submitted and interviews completed, your application enters the review period. This is arguably the most frustrating phase because you have no control and limited visibility into what's happening.

Typical review periods range from two to six weeks, though some applications take considerably longer. Traditional megabanks tend toward the longer end of this spectrum, while digital banks often approve or reject applications more quickly. A Tokyo Shoko Research survey of over 1.6 million companies found that Japan's three megabanks (MUFG, SMBC, Mizuho) collectively serve approximately 19.3% of all surveyed companies as primary banks -- their conservative approach to screening is one reason their client base skews toward established enterprises rather than newly incorporated foreign firms.

During this time, banks are conducting comprehensive background checks on both your company and its representatives. They're verifying every document, checking your company against various databases, ensuring compliance with anti-money laundering (AML) regulations, and assessing whether your business profile matches their risk tolerance.

You may be contacted for additional documentation or clarification during the review period. Respond promptly and thoroughly to any requests -- delays on your end can extend the timeline significantly.

It's acceptable to follow up periodically on your application status, but avoid being overly persistent. A polite email or phone call every two weeks is reasonable; daily contact will likely be counterproductive.

Account Activation

If your application is approved, you'll be notified to come to the bank for account activation. This final step involves signing official account opening documents, receiving your bank book (通帳, tsucho), cash cards, and setting up online banking credentials.

During activation, you'll designate authorized signatories -- individuals permitted to conduct transactions on behalf of the company. You'll also establish transaction limits, specify notification preferences, and configure any additional services like payroll processing or automatic payments.

Most banks require an initial deposit to activate the account, though the amount varies. Some banks require only a nominal deposit (¥10,000-¥50,000), while others may require substantially more, particularly if you're opening accounts with specific features or credit facilities.

Online banking setup may happen during this appointment or require separate configuration later. Banks typically issue physical security tokens or card-based authentication devices for secure access to digital banking services. Make sure you understand how to use these systems before leaving the bank, as troubleshooting later can be challenging if you don't speak Japanese.

Common Challenges and How to Overcome Them

Foreign-owned businesses face four primary challenges when opening Japanese corporate accounts: language barriers, strict KYC requirements, high rejection rates, and additional scrutiny on ownership structure -- each addressable with targeted preparation strategies.

Even with perfect preparation, opening a corporate bank account in Japan comes with inherent challenges, particularly for foreign-owned businesses. Understanding these obstacles in advance allows you to develop strategies to address them.

Language Barriers

Language presents one of the most significant practical challenges. While some banks offer limited English support, the majority of documentation, interviews, and ongoing banking operations occur in Japanese.

If you don't speak Japanese fluently, several strategies can help:

Work with professional translators: Don't rely on machine translation for critical documents. Professional translation services familiar with financial and legal terminology ensure accuracy and proper formatting.

Target banks with English support: Several banks cater specifically to international clients. GMO Aozora Net Bank, for example, provides English-language interfaces and support. SMBC has international departments with bilingual staff. Research which banks offer the level of language support you need.

Prepare bilingual materials: Create your business plan, company overview, and other key documents in both Japanese and English. This demonstrates professionalism and makes it easier for bank staff to understand your business, even if they have limited English proficiency.

Hire bilingual staff early: If possible, bring on a Japanese-speaking team member or advisor who can participate in bank meetings and handle day-to-day banking communications. This investment pays dividends throughout your business operations in Japan, not just during account opening.

Work with partners like AQ Partners: AQ Partners specializes in back office support and has a track record of opening bank accounts for multiple newly incorporated businesses in Japan.

Strict KYC (Know Your Customer) Requirements

Japanese banks are extraordinarily cautious due to strict regulatory requirements and a conservative banking culture. Know Your Customer (KYC) and Anti-Money Laundering (AML) compliance standards in Japan are among the most rigorous in the world. The Bank of Japan works alongside the FSA to maintain financial system stability, and banks face severe penalties for inadequate screening -- reinforcing why the account opening process is so thorough.

Banks are particularly vigilant about:

Source of funds: You must clearly document where your company's capital comes from. If you've received investment from foreign entities, be prepared to provide detailed information about those investors, including proof of their legitimacy and business activities.

Business legitimacy: Banks want evidence that you're running a genuine business, not using the account for money laundering or other illicit purposes. Contracts with clients or suppliers, proof of business registration in other countries, and evidence of actual business operations all help establish legitimacy.

Risk profile: Certain industries face additional scrutiny, particularly those involving cash transactions, international remittances, cryptocurrency, adult entertainment, gambling, or anything that could potentially violate Japanese laws or regulations.

To overcome these strict requirements:

- Over-document rather than under-document: Provide more information than requested to demonstrate transparency and legitimacy

- Prepare detailed explanations: Don't just submit documents -- include cover letters or explanations that contextualize the information and connect it to your business operations

- Demonstrate Japanese market commitment: Evidence of long-term commitment to the Japanese market (long-term office leases, local hiring, investment in infrastructure) helps alleviate concerns about fly-by-night operations

- Build credibility through partnerships: Letters of support or introduction from established Japanese companies, professional service providers, or industry organizations can significantly strengthen your application

Rejection and Reapplication

Not all applications succeed on the first attempt. Rejection can be disheartening, particularly after weeks of preparation and waiting, but it's not necessarily the end of the road.

Common reasons for rejection include:

- Insufficient documentation or unclear business model

- Concerns about the legitimacy or risk profile of your business

- Red flags in background checks on company representatives

- Foreign ownership structure that doesn't meet the bank's internal policies

- Industry or business activities the bank considers too high-risk

- Incomplete or inconsistent information across documents and interviews

- Visa status concerns for company representatives

If your application is rejected, try to understand the specific reasons why. Banks are rarely forthcoming with detailed explanations, but politely requesting feedback can sometimes yield useful information. Common responses include vague statements about "not meeting current account opening criteria," which is frustrating but understandable given banks' need to protect confidential internal policies.

When reapplying -- whether to the same bank or a different institution -- address whatever issues you can identify from the rejection:

- Strengthen your business documentation with more detail and evidence

- Provide additional proof of legitimate business operations

- Consider whether a different bank might be a better fit for your business profile

- Wait until you have more operational history if you applied too early in your company's lifecycle

- Ensure all company representatives have appropriate visa status and documented ties to Japan

Foreign-Owned Company Considerations

Companies with significant foreign ownership or foreign directors face additional scrutiny that purely domestic companies don't encounter.

Banks worry about several factors specific to foreign-owned businesses:

Physical presence: Banks want assurance that your company has genuine operations in Japan, not just a registered address with no real activity. Regular office hours, local employees, Japanese phone numbers and email addresses, and evidence of actual business activity all help establish your presence.

Regulatory compliance: Foreign companies must navigate both Japanese regulations and potentially home country requirements. Banks want confidence that you understand and will comply with all applicable rules.

Communication challenges: Banks prefer to communicate directly with representatives who are easily accessible in Japan and can respond quickly to requests or issues.

Repatriation concerns: There's sometimes concern that foreign-owned companies might quickly wind down operations and move money out of Japan, leaving potential issues behind.

To address these concerns:

Appoint a Japanese representative: Having at least one director or authorized representative who is a Japanese national or long-term resident significantly improves your chances. This person serves as a stable point of contact and demonstrates commitment to the Japanese market.

Demonstrate operational substance: Evidence that you're building a real business in Japan -- hiring employees, signing client contracts, investing in infrastructure -- shows banks you're not simply using the account for pass-through transactions.

Maintain transparency: Be upfront about your corporate structure, ownership, and international connections. Attempting to obscure foreign ownership typically backfires when discovered during background checks.

Consider starting with startup-friendly banks: Digital banks and specialized services like SMBC Trunk are designed specifically for foreign-owned startups and have more flexible policies and experience working with international businesses. Having a clear entity structuring strategy from the outset strengthens your application.

Costs and Fees

Corporate banking fees in Japan range from zero monthly maintenance at digital banks to over ¥3,000/month at megabanks, with international wire transfer costs of ¥2,500-¥7,000 per transaction representing the largest ongoing expense for cross-border businesses.

Banking fees in Japan vary significantly across institutions and account types. Understanding the full cost structure helps you budget appropriately and compare banks effectively.

Account Opening Fees

Unlike many Western countries where opening a business bank account is free, some Japanese banks charge initial setup fees. These range from nothing at most digital banks to ¥50,000+ at certain traditional banks, particularly if you're opening accounts with special features or international capabilities.

Minimum deposit requirements also vary. Digital banks typically require only a nominal initial deposit (¥1,000-¥10,000), while traditional banks may require ¥100,000 or more to activate the account.

Monthly Maintenance Fees

Monthly account maintenance fees depend on the bank and account type:

Digital banks like GMO Aozora Net Bank and PayPay Bank typically charge no monthly fees for basic corporate accounts, making them attractive for cost-conscious startups.

Traditional banks generally charge ¥2,000-¥3,000 per month for corporate accounts. Some offer fee waivers if you maintain minimum balances or meet certain transaction volume thresholds.

Premium accounts with additional features can cost ¥5,000-¥10,000+ monthly.

Transaction Fees

Transaction fees represent the ongoing costs you'll encounter most frequently:

Domestic transfers vary by bank, transfer method, and timing:

- Online transfers during business hours: ¥150-¥400

- Online transfers after hours or weekends: ¥250-¥600

- Branch or ATM transfers: Generally higher than online

- Same-bank transfers: Often free or heavily discounted

International wire transfers are significantly more expensive:

- Outgoing transfers: ¥2,500-¥7,000 per transaction

- Incoming transfers: ¥1,500-¥3,500 per transaction

- Correspondent bank fees: ¥1,000-¥2,500 additional

- Foreign exchange margins: 1-3% above interbank rates

ATM usage fees depend on the bank, time of day, and whether you're using your bank's ATMs or those of another institution. Many banks offer a certain number of free ATM withdrawals monthly, with fees of ¥100-¥220 per transaction thereafter.

Cash handling fees apply when depositing or withdrawing large amounts of cash. Banks may charge fees for deposits exceeding certain amounts (often starting at ¥50-100 per ¥100 bills after the first several hundred thousand yen).

Managing Your Corporate Account

Effective account management includes setting up online banking and security tokens, automating payroll and social insurance withdrawals, integrating with Japanese accounting platforms like freee or Money Forward, and evaluating multi-currency accounts for international operations.

Once your account is opened, effective management ensures smooth daily operations and helps you maximize the value of your banking relationship.

Online Banking Setup

Modern online banking is essential for efficient business operations. Most Japanese banks provide comprehensive digital banking platforms, though capabilities vary significantly.

During account activation, you'll receive login credentials and usually a physical security token or authentication device. These hardware tokens generate one-time passwords (OTPs) for secure login and transaction authorization. Guard these devices carefully -- replacing lost tokens involves paperwork and fees.

Online banking typically allows you to:

- Check account balances and transaction history

- Make domestic transfers

- Download transaction data for accounting

- Set up recurring payments

- Manage authorized users

- Request bank statements

Some banks offer mobile apps with similar functionality, though not all corporate accounts have full mobile access. Check whether your bank's mobile app supports business accounts or only personal banking.

Setting Up Payment Systems

Automating routine payments saves time and reduces the risk of missed deadlines.

Direct debit (口座振替, kouza furikae) allows vendors to automatically withdraw payments from your account. This is commonly used for:

- Office rent and utilities

- Telecommunications services

- Software subscriptions

- Insurance premiums

Setting up direct debit requires completing authorization forms for each vendor, specifying withdrawal dates and amounts. Budget carefully to ensure sufficient funds are available on withdrawal dates.

Salary payments can be automated through your bank's payroll services. You'll upload employee banking information and payment amounts, and the bank executes transfers on specified dates. This is far more efficient than manually processing individual salary transfers each month.

Automatic transfers between your own accounts help manage cash flow. For example, you might set up automatic transfers from your operating account to a separate savings account for tax reserves.

Integration with Accounting

Connecting your bank account to accounting software dramatically reduces bookkeeping burden and improves financial visibility for seamless back-office operations.

Most major Japanese accounting platforms -- freee, Money Forward Cloud, and Yayoi -- support direct bank account integration. Once connected, transactions automatically import into your accounting system, where you can categorize and reconcile them.

This integration requires:

- Enabling API access or data export features in your online banking

- Authenticating your accounting software to access bank data

- Mapping transaction categories to your chart of accounts

- Establishing regular sync schedules

Transaction data typically includes date, amount, counterparty name, and transaction type. You'll need to add descriptions or categorizations manually for proper bookkeeping, but the basic data entry is automated.

For tax compliance, maintaining accurate records of all transactions is mandatory. Integrated accounting systems make it easier to generate required reports, track deductible expenses, and prepare for tax filings and post-incorporation compliance.

Multi-Currency Accounts

If your business regularly deals with foreign currencies, multi-currency accounts can reduce conversion costs and simplify international transactions.

These accounts allow you to hold, receive, and send money in various currencies (typically USD, EUR, GBP, AUD, etc.) without converting to JPY. Benefits include:

- Avoiding repeated currency conversion fees

- Timing conversions advantageously based on exchange rates

- Simplifying accounting for international transactions

- Reducing processing time for foreign currency receipts

Not all Japanese banks offer multi-currency business accounts. Those that do often require:

- Higher minimum balances

- Additional documentation about your international business activities

- Separate application processes beyond the standard account opening

- Monthly maintenance fees for the multi-currency functionality

Consider whether transaction volumes justify the additional complexity and costs.

Tips for a Successful Application

The nine strategies below -- from starting the process 2-3 months early to applying at multiple banks in parallel -- are drawn from the experiences of hundreds of foreign companies that have successfully navigated Japan's corporate banking system.

Drawing from the experiences of hundreds of companies that have successfully opened Japanese corporate bank accounts, these strategies significantly improve your approval chances:

Start early: Begin the account opening process at least 2-3 months before you absolutely need it. Applications can take 6-8 weeks even when everything goes smoothly, and longer if you encounter problems. Don't wait until you have urgent payment deadlines.

Over-prepare documentation: Bring more documents than you think you'll need. Extra evidence of legitimate business operations, additional reference letters, supplementary financial information -- these can all help overcome hesitation from cautious bank staff.

Demonstrate genuine operations: Banks want to see that you're building a real business in Japan. Evidence of actual operations -- signed client contracts, office photos, employee information, business cards, company website -- demonstrates substance beyond just paperwork.

Consider professional services: Consultants and administrative service providers who specialize in helping foreign companies establish in Japan can be worth the investment. They understand bank requirements, can help prepare proper documentation, and sometimes have established relationships with banks that facilitate introductions.

Apply to multiple banks simultaneously: Don't put all your eggs in one basket. Apply to 2-3 banks at the same time to maximize approval chances and give yourself options if one application fails.

Ensure Japanese language capability: Either develop your own Japanese language skills, hire bilingual staff, or engage professional interpreters for bank meetings. Clear communication dramatically improves outcomes.

Maintain realistic expectations: Understanding that the process is slow and sometimes frustrating helps you remain patient and professional throughout. Banks are cautious by nature in Japan, and rushing them rarely helps.

Follow up appropriately: Stay engaged with your application without being pushy. A polite email every 2-3 weeks checking on status shows continued interest without annoying bank staff.

Be prepared to explain your business model clearly: If you can't articulate what your company does, why it exists, and how it makes money in clear, simple terms, banks will struggle to approve your application. Practice your explanation until you can deliver it conversationally in under two minutes.

Conclusion

Opening a corporate bank account in Japan represents a significant milestone in establishing your business operations in the country. While the process can be lengthy, documentation-intensive, and sometimes frustrating, successful completion provides the financial infrastructure necessary for conducting business in the Japanese market.

The key to success lies in thorough preparation, realistic expectations, and strategic selection of banking partners. Understand that Japanese banks prioritize caution and compliance over speed and convenience. Rather than fighting this reality, work within it by providing comprehensive documentation, demonstrating genuine business substance, and choosing banks that align with your company's profile and needs.

Remember that your initial bank choice isn't necessarily permanent. Many successful companies start with accessible digital banks to get operations running, then later add accounts at traditional megabanks as they grow and build track records. Others maintain multiple accounts from the start to access different features and services from different institutions.

Most importantly, view account opening as the beginning of a long-term banking relationship rather than a one-time transaction. Japanese business culture values sustained relationships, and banks are no exception. Maintain active accounts, communicate regularly with your bank representatives, stay compliant with all requirements, and gradually build trust that opens doors to additional financial services as your business grows.

With patience, preparation, and persistence, you'll successfully navigate the corporate banking landscape in Japan and establish the financial foundation your business needs to thrive in this unique and rewarding market.

Frequently Asked Questions

How long does it take to open a corporate bank account in Japan?

The timeline varies significantly by bank and your specific circumstances. Digital banks like GMO Aozora Net Bank can approve applications in 2-3 weeks for straightforward cases. Traditional megabanks typically take 4-8 weeks, sometimes longer. Allow at least 2-3 months from starting your application to having a fully operational account with all desired features activated.

Can I open an account before registering my company?

No. Japanese banks require proof of registered legal entity status before opening corporate accounts. You must complete company registration with the Legal Affairs Bureau first, obtain your registration certificate, and register your company seal before approaching banks.

What if I don't speak Japanese?

Language is challenging but not insurmountable. Options include: targeting banks with English support (GMO Aozora Net Bank, SMBC international departments), bringing professional interpreters to meetings, hiring bilingual staff or consultants, and preparing all materials in both Japanese and English. Many foreign-founded companies successfully open accounts despite limited Japanese ability.

Can branch offices of foreign companies open accounts?

Yes, but the process can be more complex than for locally incorporated entities. You'll need extensive documentation about the parent company, proof of branch registration in Japan, and clear explanations of how the branch operates relative to the parent company. Some banks are more comfortable with branch offices than others.

How many corporate accounts should my business have?

Most businesses benefit from at least two accounts: a primary operating account for general business transactions, and a separate account for tax reserves or payroll. Some companies maintain additional accounts for specific purposes (project-specific accounts, investment accounts, accounts at multiple banks for relationship diversity). Start with one or two and expand as needed.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.