Tax Audits in Japan: What Foreign Companies Should Expect

A tax audit in Japan — formally called a tax examination (税務調査, zeimu chosa) — is an investigation conducted by the National Tax Agency (NTA) or regional tax bureaus to verify that a company's tax returns accurately reflect its taxable income, deductions, and obligations. For foreign companies operating through a Japanese subsidiary, branch office, or permanent establishment, these examinations carry heightened scrutiny. The NTA conducts over 74,000 corporation tax examinations annually, with foreign-owned entities disproportionately selected for transfer pricing audits. Understanding the types of examinations, common triggers, and penalty structures is essential for any foreign company doing business in Japan.

Key Takeaways

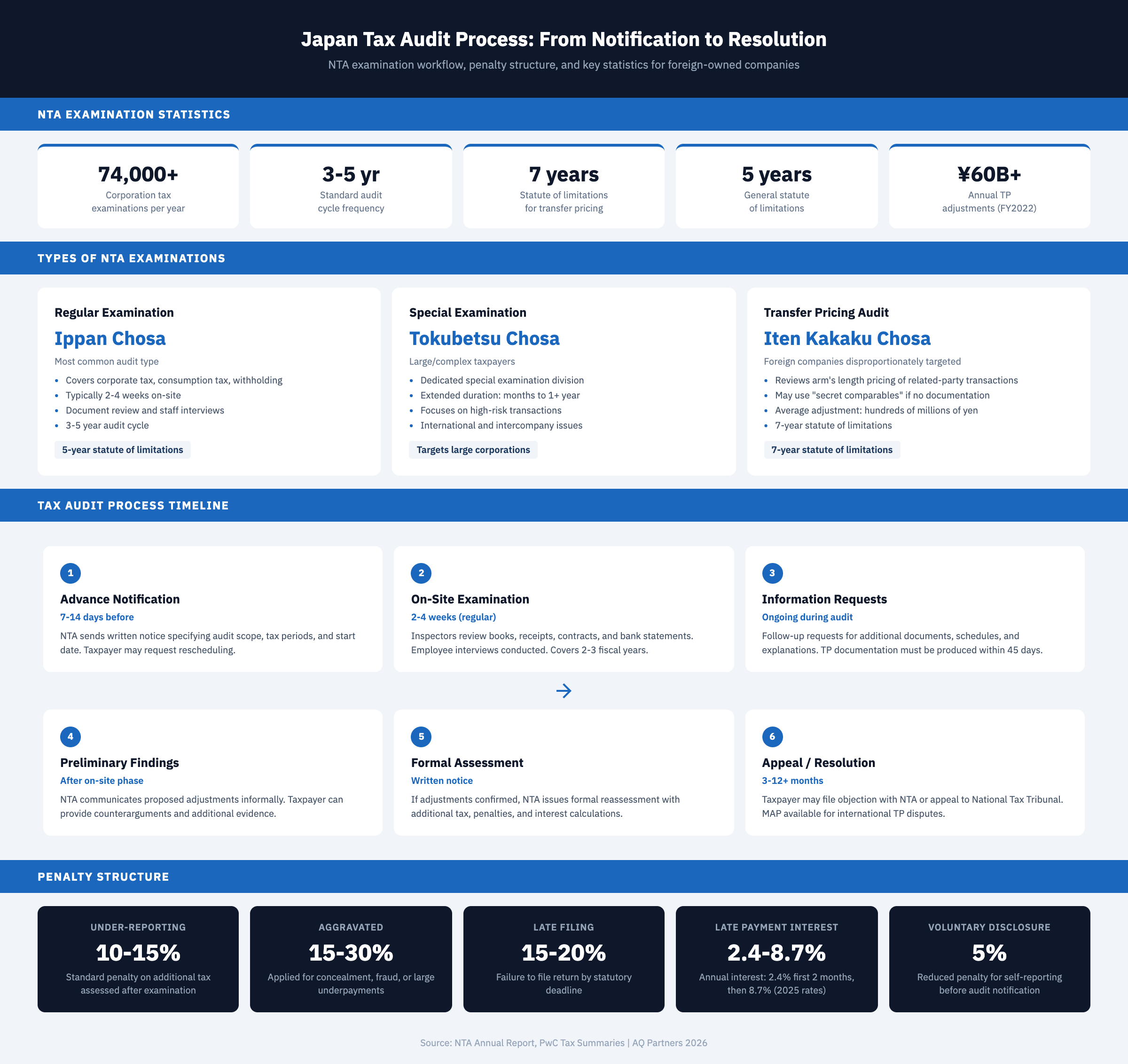

- The NTA audits corporations on a 3-to-5-year cycle — over 74,000 corporation tax examinations are conducted annually, and the cycle shortens for companies with significant international transactions or prior compliance issues.

- Foreign companies face elevated transfer pricing scrutiny — the NTA concluded approximately 200 transfer pricing examinations with adjustments in FY2022, totaling over ¥60 billion in corrections, with foreign-owned subsidiaries representing a disproportionate share of targets.

- Advance notification is legally required before most audits begin — the NTA must provide written notice specifying the audit scope, tax periods, and scheduled dates, giving taxpayers time to prepare documentation and engage advisors.

- Penalties range from 5% for voluntary disclosure to 30% for aggravated under-reporting — late payment interest accrues at 2.4% for the first two months and 8.7% thereafter (2025 rates), compounding the financial impact of any adjustment.

- Maintaining contemporaneous documentation is the single most effective audit defense — companies that can produce organized records, transfer pricing Local Files, and supporting schedules within the NTA's 45-day window significantly reduce the risk of adverse findings.

How Tax Audits Work in Japan

Japan's tax examination system is administered by the NTA and its 12 regional tax bureaus, which select companies for audit based on risk scoring, industry benchmarks, and filing history — not random selection.

The NTA's examination division uses a risk-based approach to prioritize audit targets. Each corporation's tax return is scored against industry norms, prior-year trends, and known risk indicators. Companies flagged for review receive a formal advance notification (事前通知, jizen tsuchi) specifying the taxes under examination, the fiscal years covered, and the proposed start date. Under Japan's National Tax Agency procedural rules, taxpayers have the right to request a rescheduling of the audit start date, though they cannot refuse an examination entirely.

The examination typically covers two to three fiscal years and involves on-site review of accounting records, bank statements, contracts, invoices, and employee interviews. According to PwC's Worldwide Tax Summaries, corporate tax audits occur in 3-to-5-year cycles, though this interval shortens for companies with significant tax matters, industry-wide reviews, or media-reported transactions. Once an audit of a specific period concludes, a second examination of the same period is generally prohibited unless new information surfaces.

Types of NTA Examinations

The NTA conducts three primary types of tax examinations — regular, special, and transfer pricing — each with distinct scope, duration, and implications for foreign companies.

Regular examinations (一般調査, ippan chosa) cover corporate income tax, consumption tax, and withholding obligations, typically lasting two to four weeks on-site with a five-year statute of limitations. Special examinations (特別調査, tokubetsu chosa) are reserved for large or complex taxpayers, conducted by dedicated divisions within regional tax bureaus. These can extend for months to over a year, focusing on international operations, restructurings, and intercompany financing.

Transfer pricing examinations (移転価格調査, iten kakaku chosa) are particularly significant for foreign companies. The NTA's transfer pricing division reviews whether related-party transactions comply with the arm's length principle under Articles 66-4 and 68-88 of the Special Taxation Measures Act. Approximately 200 transfer pricing examinations resulted in adjustments in FY2022, with total corrections exceeding ¥60 billion. The statute of limitations for transfer pricing extends to seven years. Foreign-owned subsidiaries are disproportionately targeted because their cross-border transactions create pricing risks that the NTA's algorithms flag.

| Examination Type | Japanese Term | Typical Duration | Statute of Limitations | Primary Focus | Common Targets |

|---|---|---|---|---|---|

| Regular Examination | 一般調査 (Ippan Chosa) | 2-4 weeks | 5 years | Corporate tax, consumption tax, withholding | All corporations on cycle |

| Special Examination | 特別調査 (Tokubetsu Chosa) | Months to 1+ year | 5-7 years | Complex transactions, restructurings | Large corporations |

| Transfer Pricing Audit | 移転価格調査 (Iten Kakaku Chosa) | 6-18 months | 7 years | Arm's length pricing of related-party transactions | MNEs with cross-border transactions |

| Desk Audit | 簡易調査 (Kan'i Chosa) | 1-2 weeks | 5 years | Specific line items or discrepancies | SMEs, simple issues |

| Criminal Investigation | 査察 (Sasatsu) | 1-2 years | No limit (criminal) | Tax evasion, fraud | Cases with suspected willful evasion |

| Consumption Tax Audit | 消費税調査 (Shouhizei Chosa) | 2-3 weeks | 5 years | Input credits, invoice compliance | Companies with large input tax claims |

Common Audit Triggers for Foreign Companies

Foreign-owned companies in Japan face specific audit triggers that domestic companies do not — particularly around transfer pricing, permanent establishment issues, and cross-border payments.

The NTA's risk-scoring system flags several patterns that are common among foreign-owned entities. Large or recurring related-party transactions with overseas parents or affiliates are the primary trigger for transfer pricing scrutiny. The NTA cross-references reported intercompany prices against industry benchmarks and publicly available financial data to identify outliers. Companies reporting consistently low margins or losses despite being part of profitable global groups attract particular attention — the NTA questions why a Japanese subsidiary would sustain losses while its parent generates strong returns.

Royalty payments, management fees, and intercompany service charges are closely examined for arm's length compliance. Significant year-over-year fluctuations in taxable income, entity restructurings, and late or amended filings also elevate audit risk. According to JETRO's guidance for foreign companies, entities with permanent establishments must allocate costs and expenses fairly, and failure to demonstrate proper allocation is a frequent finding.

The NTA also receives Country-by-Country Reports through automatic exchange agreements with over 80 jurisdictions, enabling direct comparison of a Japanese entity's results against its global group's profitability.

The Examination Process

A standard NTA tax examination follows a structured six-phase process from advance notification through resolution, typically spanning three to six months for regular audits and up to 18 months for transfer pricing cases.

The process begins with a formal advance notification delivered to the taxpayer (or its tax agent) specifying the scope of examination, the tax types and fiscal years under review, and the proposed start date. The taxpayer has the right to request rescheduling, and most companies use this window to organize records and brief their advisors.

During the on-site phase, NTA inspectors review general ledgers, bank statements, contracts, invoices, receipts, and payroll records. They interview accounting staff and management to verify that recorded transactions reflect economic substance. For transfer pricing examinations, inspectors request the Local File, functional analysis, and benchmarking studies — documentation that must be produced within 45 days.

After the on-site phase, the NTA communicates preliminary findings informally, giving the taxpayer an opportunity to provide counterarguments. If adjustments are confirmed, the NTA issues a formal reassessment with additional tax, penalties, and interest. The taxpayer may accept the assessment, file for reconsideration, or appeal to the National Tax Tribunal (国税不服審判所). For transfer pricing disputes, the Mutual Agreement Procedure (MAP) under tax treaties provides an additional mechanism — Japan's average MAP resolution time is 30.1 months, slightly faster than the OECD average of 32 months.

| Phase | Timeline | Key Activities | Taxpayer Actions |

|---|---|---|---|

| 1. Advance Notification | 7-14 days before start | Written notice of scope, periods, dates | Review notice, engage advisor, request rescheduling if needed |

| 2. On-Site Examination | 2-4 weeks (regular) | Document review, ledger analysis, interviews | Provide access to records, designate liaison, prepare meeting rooms |

| 3. Information Requests | Ongoing during audit | Follow-up document requests, schedule clarifications | Respond promptly (45-day deadline for TP documentation) |

| 4. Preliminary Findings | After on-site phase | Informal communication of proposed adjustments | Submit counterarguments, additional evidence, technical memos |

| 5. Formal Assessment | Written reassessment | Official notice with tax, penalties, interest calculations | Review assessment, decide whether to accept or dispute |

| 6. Dispute Resolution | 3-12+ months | Reconsideration, NTT appeal, MAP for TP cases | File objection within 3 months; MAP request to competent authority |

Penalties and Dispute Resolution

Japan's penalty regime for tax non-compliance includes under-reporting surcharges of 10-15%, aggravated penalties up to 30%, late filing penalties of 15-20%, and late payment interest that compounds at annual rates of 2.4% to 8.7%.

The penalty structure is designed to incentivize voluntary compliance and early disclosure. If a taxpayer voluntarily files an amended return before receiving audit notification, the under-reporting penalty is reduced to 5%. Once the NTA issues an audit notification, the reduced rate rises to 10-15% depending on the amount of additional tax. Aggravated under-reporting penalties of 15-30% apply when the NTA determines that the taxpayer concealed income, fabricated records, or when the underpayment exceeds specified thresholds. According to PwC's Japan tax administration guide, late payment interest accrues at 2.4% per annum for the first two months after the due date and 8.7% thereafter (2025 rates).

Transfer pricing adjustments create double taxation when the NTA increases the Japanese entity's taxable income without a corresponding reduction abroad. The Mutual Agreement Procedure (MAP) under bilateral tax treaties is the primary resolution mechanism — Japan had 159 MAP cases in FY2023, with an average resolution time of 30.1 months according to OECD statistics. Companies can also pursue Advance Pricing Arrangements (APAs) to eliminate future dispute risk. Bilateral APAs provide the strongest protection against double taxation.

The formal dispute pathway begins with a request for reconsideration filed with the NTA within three months of the assessment notice. If unsatisfied, the taxpayer may appeal to the National Tax Tribunal within one month. Judicial review is available as a final recourse, though tax litigation in Japan typically takes two to four years.

How to Prepare for a Tax Audit

Proactive preparation — including maintaining organized records, preparing transfer pricing documentation in advance, and establishing a relationship with a qualified tax advisor — is the most effective strategy for minimizing audit risk and adverse findings.

Foreign companies should ensure that all accounting records are maintained in Japanese or have certified translations available, as NTA inspectors conduct examinations in Japanese. General ledgers, sub-ledgers, bank reconciliations, fixed asset registers, and payroll records should be organized by fiscal year and readily accessible. For companies engaged in related-party transactions, transfer pricing documentation — including the Local File, functional analysis, and benchmarking study — should be prepared contemporaneously rather than assembled after an audit notice arrives.

Companies filing on the blue form tax return (青色申告) benefit from enhanced procedural protections during audits, including the right to carry forward losses for up to 10 years and specific documentation requirements that, when met, provide stronger audit defense. Maintaining blue form status requires accurate bookkeeping and timely filing — precisely the disciplines that also reduce audit risk.

Designating an internal audit liaison — typically a senior finance or accounting manager — ensures consistent communication with NTA inspectors and prevents ad hoc employee interviews from creating confusion. Companies should also conduct internal pre-audit reviews, comparing their filing positions against industry norms and identifying potential areas of NTA interest before the examination begins. Understanding the Japan tax filing calendar and ensuring all returns are filed accurately and on time is the foundational step in audit preparation — late or amended filings are among the most common triggers for NTA scrutiny.

Navigating Tax Audits as a Foreign Company in Japan

Foreign-owned companies face unique challenges during Japanese tax audits, including language barriers, unfamiliarity with NTA procedures, and the complexity of defending cross-border transactions.

The NTA does not conduct examinations in English, and all documentation must be presented in Japanese. Engaging a bilingual licensed tax accountant (税理士, zeirishi) who serves as the company's tax agent is essential — the tax agent receives audit notifications, communicates with inspectors on the company's behalf, and provides technical arguments in Japanese. Foreign companies that rely solely on home-country finance teams often struggle because personnel familiar with underlying transactions cannot communicate directly with inspectors.

The NTA's approach to corporate income tax calculations differs from many Western jurisdictions. Deductions that are standard elsewhere — such as management fees, head office cost allocations, and intercompany interest — may be challenged if the company cannot demonstrate arm's length pricing. The NTA takes a substance-over-form approach, examining whether intercompany charges correspond to genuine economic activity in Japan. Building audit readiness into operations from day one, as outlined in Japan's corporate tax compliance framework, dramatically reduces both the risk of selection and the severity of findings.

AQ Partners helps foreign companies in Japan build audit-ready back office operations — from bookkeeping and tax filing to transfer pricing documentation support. Contact our team to discuss how we can help your company prepare for NTA examinations with confidence.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.