Japan Salary Structure: Pay, Allowances & Bonuses

Key Takeaways

- Japan salary packages have 3–5 components beyond base pay — each with distinct tax treatment, social insurance implications, and legal status under the Labour Standards Act. Understanding each component is essential for accurate cost modelling and compliance.

- Base salary (基本給 kihon kyuyo) drives social insurance calculations — the standardised monthly remuneration brackets used by the Ministry of Health, Labour and Welfare (MHLW) are based primarily on base salary, making the base figure a critical variable in total employment cost.

- Allowances vary significantly in tax and social insurance treatment — commuting allowances are tax-exempt up to ¥150,000 per month, while housing and family allowances are fully taxable. Misclassifying allowances creates exposure with both the National Tax Agency (NTA) and social insurance authorities.

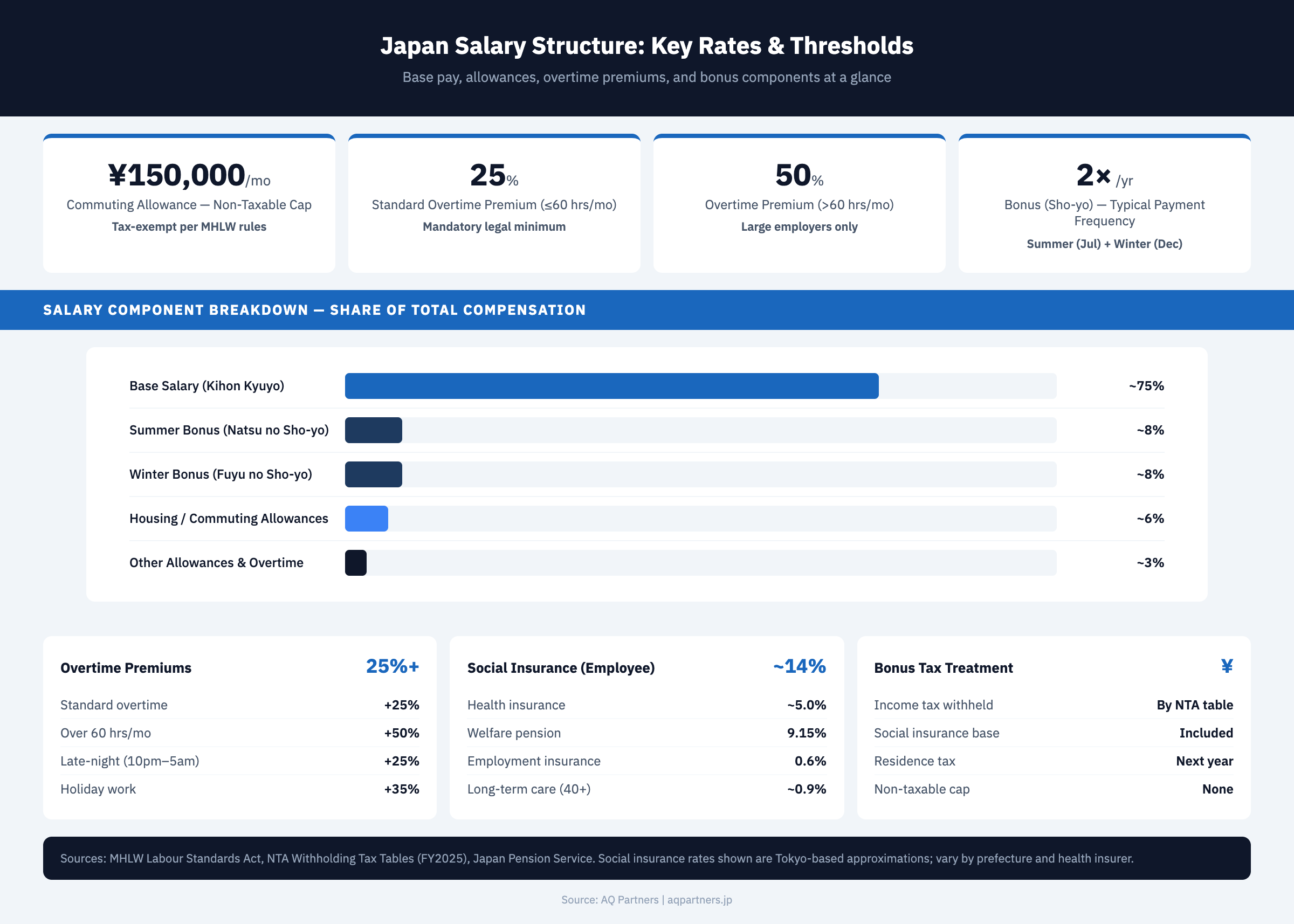

- Overtime pay premiums are mandated by law and non-negotiable — the Labour Standards Act sets minimum premiums starting at 25% for standard overtime and rising to 60% for late-night holiday work. Employers must file a 36-agreement before requiring any overtime.

- Bonuses are discretionary in law but expected in practice — approximately 80% of Japanese companies with 30 or more employees pay summer and winter bonuses, and they are subject to full social insurance contributions and special income tax withholding rates.

Japan salary packages look straightforward on the surface — a monthly salary, a bonus twice a year, and a few allowances. In practice, each of those components is governed by a distinct set of rules under the Labour Standards Act, the Income Tax Act, and the social insurance legislation administered by the MHLW. Getting the structure right matters not just for compliance but for accurate cost budgeting, competitive positioning in the talent market, and payroll processing efficiency. This post covers every major component of a Japanese salary package, its legal basis, and the tax and social insurance treatment that applies. For a complete overview of Japan payroll obligations, see our Japan payroll guide.

How Japanese Salary Packages Are Structured

Japan salary packages typically have 3–5 distinct components beyond base pay, each with different tax, social insurance, and legal treatment. Unlike many Western countries where total compensation is a single figure, Japanese payslips itemise every component.

A standard Japanese payslip — the 給与明細 (kyuyo meisai) — lists each component of compensation separately. The typical structure for a full-time employee at a mid-to-large Japanese company includes: base salary (基本給), a set of named allowances (手当), overtime pay where applicable (残業代), and a separate bonus payment issued twice per year (賞与). For longer-tenured employees, a retirement allowance accrues over the course of their career (退職金).

This itemised structure is not merely a payslip convention. It reflects the fact that each component is governed by different rules. Base salary sets the reference point for social insurance contributions. Some allowances are excluded from that calculation while others are included. Bonuses are subject to social insurance contributions but taxed at a different rate to regular salary. Retirement allowances receive preferential income tax treatment under the PwC Japan Tax Summaries framework, reflecting their nature as deferred compensation for long service.

For foreign companies hiring in Japan, this structure has direct implications for cost modelling. A compensation offer that appears competitive based on base salary may be significantly more expensive once allowances, social insurance on bonuses, and retirement allowance accrual are factored in. It also has implications for offer letters — employment contracts in Japan should specify each allowance separately, as changes to named compensation components require formal notification under the Labour Standards Act.

Base Salary (基本給 Kihon Kyuyo)

Base salary is the fixed monthly amount paid to an employee regardless of performance, hours, or output. It forms the primary basis for social insurance calculations under the standardised monthly remuneration (標準報酬月額) bracket system and cannot be reduced without formal agreement and legal notification.

Kihon kyuyo is the foundation of the Japanese compensation structure. It is a fixed monthly amount, specified in the employment contract, that does not vary with hours worked, sales results, or other performance metrics. Variable performance pay in Japan is typically handled separately — either through the bonus mechanism or through role allowances — rather than by making base salary itself variable.

The significance of base salary extends beyond its face value. Japan's social insurance system uses a standardised monthly remuneration (標準報酬月額) bracket system to determine employer and employee contributions to health insurance and the Employees' Pension Insurance scheme. The bracket is determined each year between April and June based on the actual remuneration received by each employee, with the resulting grade taking effect from September. Because most allowances are included in this calculation alongside base salary, increases to allowances as well as base salary can shift an employee into a higher remuneration bracket, increasing contribution costs for both parties.

According to MHLW Basic Survey on Wage Structure data, the average monthly scheduled cash earnings for full-time workers in Japan across all industries was approximately ¥307,000 in recent survey years, with significant variation by industry, company size, and seniority. Technology sector roles and financial services roles at large companies typically carry base salaries considerably above this average.

Salary reviews in Japan are predominantly annual, with April being by far the most common review month — a legacy of the Japanese fiscal year and the April graduation and new-hire intake cycle. Mid-year reviews do occur, particularly at foreign-affiliated companies, but they remain the exception rather than the norm. Any reduction to base salary requires written employee consent and, in certain circumstances, notification to the relevant labour standards inspection office under Article 89 of the Labour Standards Act. The JETRO Business Setup Guide provides practical background on employment contract requirements that apply to base salary terms.

Allowances — Taxable vs Tax-Exempt

Allowances are the most varied and legally nuanced component of Japanese compensation. Their tax and social insurance treatment differs significantly by type, and misclassification creates exposure with both the NTA and social insurance authorities.

Japanese employers routinely offer a range of named allowances alongside base salary. These allowances serve practical purposes — reimbursing commuting costs, offsetting housing expenses, supporting employees with dependants — but they also carry distinct tax and social insurance treatment that must be applied correctly in payroll processing. The table below summarises the eight most common allowances.

| Allowance | Japanese Term | Tax Treatment | Social Insurance |

|---|---|---|---|

| Commuting | 通勤手当 tsūkin teate | Tax-exempt up to ¥150,000/month | Excluded from standard monthly remuneration |

| Housing | 住宅手当 jūtaku teate | Fully taxable | Included in remuneration |

| Family/dependent | 家族手当 kazoku teate | Fully taxable | Included in remuneration |

| Meal | 食事手当 shokuji teate | Tax-exempt if within limits | Excluded if within limits |

| Overtime | 残業代 zangyo dai | Taxable | Included in remuneration |

| Role/position | 役職手当 yakushoku teate | Taxable | Included in remuneration |

| Skills/qualification | 資格手当 shikaku teate | Taxable | Included in remuneration |

| Remote work | テレワーク手当 | Partially exempt (equipment costs) | Excluded if genuine expense |

The commuting allowance warrants particular attention. The ¥150,000 monthly tax exemption cap is generous for most employees using public transport, but for employees claiming private vehicle commuting costs, the exempt amount is determined by a separate distance-based calculation. Amounts above the relevant exemption ceiling are treated as taxable income. The NTA publishes updated guidance on commuting allowance limits annually.

Housing allowances paid as a cash supplement to base salary — as opposed to company-provided housing with a nominal employee contribution — are fully taxable and included in standardised monthly remuneration. This distinction matters for foreign companies that are accustomed to using housing allowances as a tax-efficient benefit: in Japan, a cash housing allowance does not carry the same tax efficiency as company-provided accommodation arrangements.

Remote work allowances have grown in usage since 2020 and occupy a nuanced position. Where the allowance is genuinely reimbursing documented expenses — internet costs, equipment purchases, utility increases attributable to home working — it may be treated as a non-taxable expense reimbursement and excluded from social insurance remuneration. Where it functions as a fixed cash supplement with no documented expense basis, it is likely to be treated as taxable income.

For employers using MoneyForward Cloud Payroll or similar domestic payroll platforms, each allowance type should be configured with the correct tax and social insurance classification from the outset. Reconfiguring allowance classifications retrospectively — and recalculating prior periods — is operationally complex and creates reconciliation work with the Japan Pension Service.

Overtime Pay Rules

Japan's Labour Standards Act mandates minimum overtime premium rates for all hours worked beyond the statutory limit. These premiums are non-negotiable and cannot be contracted out of — employers that pay below the statutory rate face back-pay liability and potential criminal penalties.

Japan's standard working hours under the Labour Standards Act are 8 hours per day and 40 hours per week. Hours worked beyond these limits are overtime and must be compensated at the following minimum premium rates:

- Standard overtime (beyond 8 hours/day or 40 hours/week): 25% premium on the hourly rate

- Late-night overtime (work between 10pm and 5am): 25% premium, applied cumulatively with the standard overtime premium where both conditions apply

- Holiday work (statutory rest days): 35% premium

- Late-night holiday work: 60% premium (35% holiday + 25% late-night)

- Monthly overtime exceeding 60 hours: 50% premium (applicable to employers with more than 50 employees; smaller employers were brought into scope from April 2023)

Before requiring any employee to work overtime, an employer must file a 36-agreement (三六協定, sanroku kyotei) with the local Labour Standards Inspection Office. The 36-agreement — named after Article 36 of the Labour Standards Act — sets out the maximum number of overtime hours that may be required and the departments or employee categories to which the agreement applies. Without a valid 36-agreement in place, requiring overtime is a violation of the Labour Standards Act, regardless of whether the employee is willing to work the additional hours.

The 2019 working style reform legislation introduced statutory caps on overtime under the 36-agreement framework: a general limit of 45 hours per month and 360 hours per year, with special circumstances provisions allowing up to 100 hours in a single month and 720 hours per year provided monthly overtime does not average more than 80 hours over a two- to six-month period. These caps apply to most industries, with some sector-specific phase-in periods that are now complete.

For foreign companies managing Japan HR compliance within a broader international workforce structure, overtime tracking and the 36-agreement filing process are among the most common areas where gaps occur. For further guidance, see our post on Japan HR compliance strategies for global teams.

Bonuses (賞与 Sho-yo)

Bonuses in Japan are discretionary in law but deeply embedded in practice — they form a significant portion of total annual compensation and carry specific social insurance and income tax treatment that must be applied correctly in payroll processing.

Japan's bonus culture operates on a twice-yearly cycle. The summer bonus (夏季賞与) is typically paid in June or July, and the winter bonus (冬季賞与) in December. For employees at large and mid-size Japanese companies, each bonus payment is commonly equivalent to 1–2 months of base salary, though the amount varies by employer, industry, and individual performance assessment. According to MHLW survey data, approximately 80% of companies with 30 or more employees pay bonuses.

From a legal standpoint, the Labour Standards Act does not require employers to pay bonuses. Unlike base salary, a bonus obligation only exists if it is explicitly promised in the employment contract, the company's rules of employment (就業規則, shugyo kisoku), or a collective agreement. In practice, however, removing or substantially reducing an established bonus at a Japanese company carries significant legal and reputational risk, and courts have in some cases treated customary bonus payments as quasi-contractual obligations.

The payroll treatment of bonuses differs from that of monthly salary in two important respects. First, social insurance contributions — health insurance and pension — are calculated on the actual bonus amount with a special bonus-specific contribution rate, and employer and employee contributions are both due on the full bonus payment. This means that a bonus of ¥600,000 will attract significant additional employer social insurance cost on top of the gross bonus amount. Second, income tax on bonuses is withheld at a special bonus withholding rate published by the NTA, calculated by reference to the previous month's regular salary and the employee's dependant status, rather than the standard monthly withholding table. Payroll teams must apply the correct table to avoid systematic under- or over-withholding that compounds through the year and complicates the nenmatsu chosei year-end adjustment.

For a full breakdown of payroll compliance obligations including social insurance contribution rates and the nenmatsu chosei process, see our post on Japan payroll compliance: social insurance and nenmatsu chosei.

Retirement Allowance (退職金 Taishoku-kin)

Retirement allowance is not legally required in Japan, but it is offered by approximately 75% of large Japanese companies and is a significant factor in talent retention for long-tenured employees. It must be factored into total compensation budgeting and carries preferential income tax treatment under the Income Tax Act.

Taishoku-kin is a lump-sum payment made to an employee upon retirement or departure from the company. Unlike a pension, it is typically paid as a single amount at the point of separation rather than as an ongoing annuity, though some larger companies operate both a lump-sum retirement allowance and a corporate defined-contribution pension plan (企業型DC) alongside each other.

The amount of retirement allowance is determined by the employer's retirement allowance regulation (退職金規程), which specifies the calculation formula. The two most common approaches are:

- Fixed amount per year of service: A multiple of base salary at the time of retirement, multiplied by years of service and adjusted by a coefficient that reflects the reason for departure (voluntary resignation typically attracts a lower coefficient than mandatory retirement at age).

- Point-based formula: Employees accumulate points each year based on their grade, role, and performance rating. The total points at departure are converted to a yen amount using a fixed point value. This approach provides more granular differentiation of the retirement benefit based on career progression.

The income tax treatment of retirement allowances is preferential compared to regular income. The taxable amount is calculated by deducting a substantial retirement income deduction (退職所得控除) — which increases with years of service — and then halving the remainder. The result is taxed at the applicable marginal rate, but because of the deduction and halving, the effective tax rate on retirement allowances is typically far lower than on equivalent regular income. This tax preference reflects the government's policy intent to encourage long-term employment.

For finance teams, the accounting treatment of retirement allowances is a further consideration. Under J-GAAP, companies that offer retirement allowances are required to record an accrued liability based on the present value of the estimated future obligation. This accrual represents a real cost that should be included in headcount cost modelling from the point of hire, not only recognised when the allowance is actually paid. The accrual methodology and discount rate assumptions are specified under the relevant Japanese accounting standards.

Structuring Compensation for Foreign Hires

Foreign companies hiring in Japan — whether Japanese nationals, expatriates, or non-Japanese local hires — frequently need to reconcile Japan's itemised salary structure with global compensation frameworks. The differences in structure, not just in amounts, are the primary source of complexity.

Global compensation frameworks used by multinational companies — total cash, total remuneration, or band-based structures — typically express compensation as a single annual or monthly figure. Japan's itemised structure requires that figure to be disaggregated into legally distinct components, each with its own employment contract status and payroll treatment. This is not merely an administrative exercise: the classification of each component determines tax and social insurance treatment and affects the employee's net take-home pay.

For foreign nationals relocating to Japan, several common adjustments apply:

- Housing allowance: Where the employee's home country package included a company-provided accommodation or housing benefit, foreign companies often replicate this in Japan as a cash housing allowance. As noted above, cash housing allowances are fully taxable and included in social insurance remuneration — which may make company-leased accommodation with an employee contribution a more tax-efficient structure in some cases.

- Cost-of-living supplement: For expatriates seconded to Japan from lower-cost locations, a cost-of-living differential supplement is sometimes included. This is typically structured as a taxable allowance and must be included in the employment contract or secondment letter.

- International health insurance top-up: Employees enrolled in Japan's national health insurance or Employees' Health Insurance scheme may also hold international health insurance policies through their employer for coverage outside Japan. The employer's premium contribution to such a policy may be treated as a taxable benefit in kind depending on the structure of the policy.

- Retirement allowance alignment: Foreign companies may choose not to offer a Japanese-style retirement allowance if the employee is not expected to serve for the full tenure that makes such a benefit meaningful. Where this is the case, the employment contract and rules of employment should be explicit about the absence of a retirement allowance entitlement to avoid ambiguity.

For more detail on the specific payroll and compliance requirements that apply to non-Japanese employees and expatriates working in Japan, see our post on Japan payroll for foreign employees.

How AQ Partners Can Help

AQ Partners provides payroll and compensation structuring support for foreign companies operating in Japan. Whether you are designing a compensation package for your first Japan hire, aligning a global compensation framework with Japan's itemised salary structure, or reviewing existing allowance classifications for tax and social insurance compliance, we provide structured advisory support backed by in-country payroll expertise.

Our services cover employment contract drafting and review, compensation structure design, allowance classification, overtime compliance, bonus payroll processing, retirement allowance regulation drafting, and ongoing payroll administration. We work with companies at every stage — from pre-hire cost modelling through to ongoing monthly payroll and year-end adjustment.

Need help structuring compensation for your Japan team? Contact AQ Partners →

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.