Bridging the Gap: Key Differences in Japanese and International Accounting

Key Takeaways

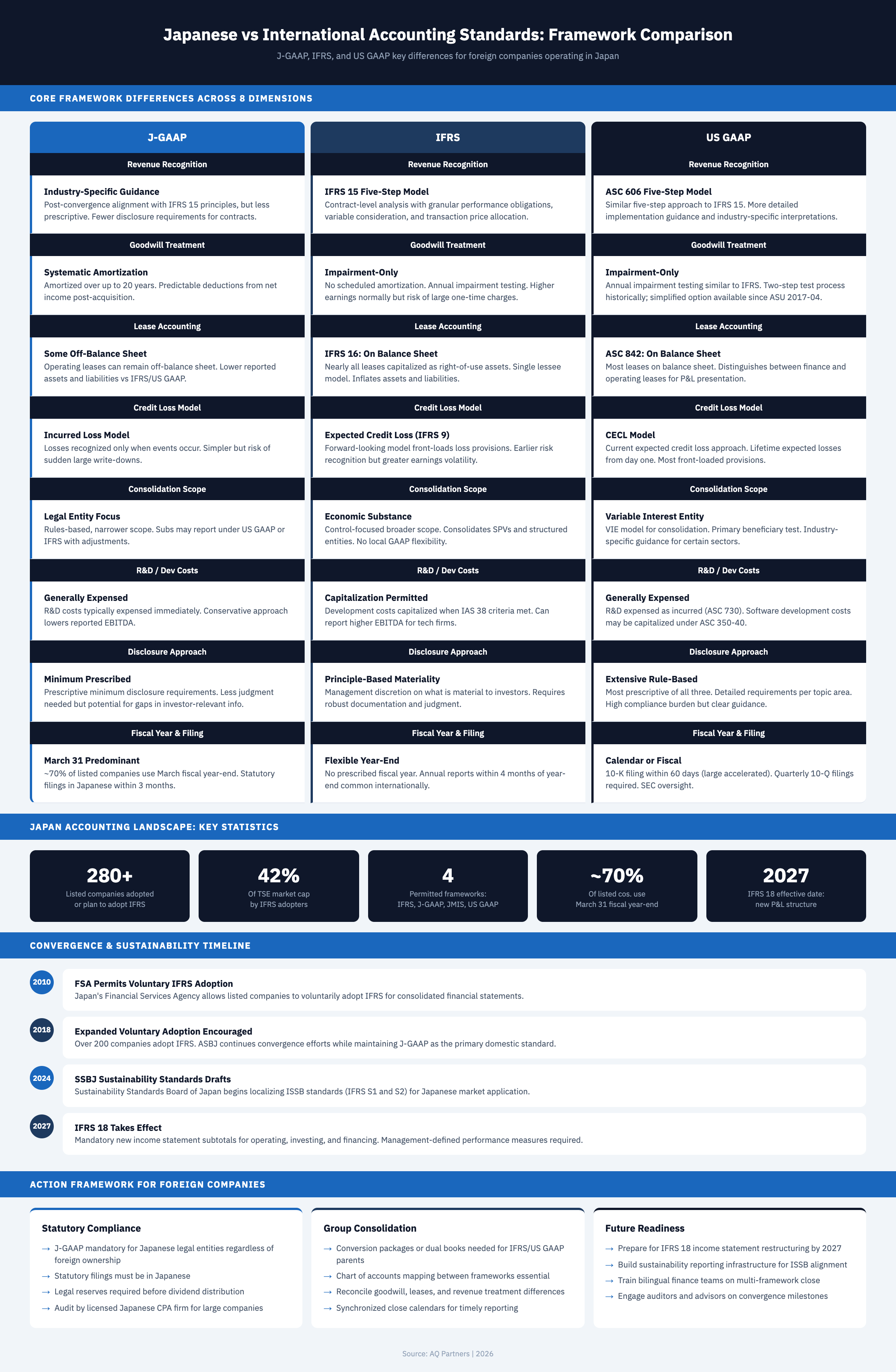

- J-GAAP is mandatory for all Japanese legal entities regardless of foreign ownership -- statutory filings, tax calculations, and dividend capacity are all determined by J-GAAP financials. Even subsidiaries of IFRS or US GAAP parent companies must prepare and retain J-GAAP statutory books under the Companies Act.

- Over 280 listed companies in Japan now report under IFRS, representing approximately 42% of Tokyo Stock Exchange market capitalization -- voluntary IFRS adoption has expanded steadily since the Financial Services Agency first permitted it in 2010, though Japan maintains a unique four-framework system that also includes JMIS and US GAAP.

- Goodwill treatment creates the most significant profit profile difference between J-GAAP and international standards -- J-GAAP mandates systematic amortization over up to 20 years, producing predictable deductions, while both IFRS and US GAAP use impairment-only testing that can result in higher steady-state earnings but large one-time charges.

- Foreign subsidiaries must reconcile dual reporting requirements between local J-GAAP statutory books and group IFRS or US GAAP consolidation packages -- differences in lease capitalization, revenue recognition, credit loss provisioning, and consolidation scope all create material adjustments that demand careful mapping and documentation.

- IFRS 18 takes effect in 2027, introducing mandatory new income statement subtotals and management-defined performance measures -- companies should prepare for restructured primary financial statements and enhanced disclosure requirements as Japan continues aligning with international reporting standards and ISSB sustainability frameworks.

Bridging the Gap: Key Differences in Japanese and International Accounting

Navigating the differences between Japanese accounting and international standards is crucial for foreign founders, startup teams, and global companies looking to expand into Japan. This challenge goes beyond language and procedures -- it is about reconciling two distinct worlds of financial logic and regulation. According to the IFRS Foundation's jurisdiction profile for Japan, over 280 listed companies now voluntarily report under IFRS, yet J-GAAP remains the mandatory standard for statutory reporting by all Japanese legal entities. This article explores what Japanese GAAP (J-GAAP) means compared to IFRS and US GAAP, how these standards impact compliance, and what global teams must do for seamless, compliant operations.

What Japanese Accounting vs. International Standards Means Operationally

Operational success in Japan requires understanding that J-GAAP, IFRS, and US GAAP differ fundamentally in framework philosophy, regulatory scope, and disclosure expectations -- and these differences directly shape reporting obligations, system requirements, and strategic decisions for cross-border companies.

Operational success begins with understanding the distinctions among J-GAAP, IFRS, and US GAAP -- including their frameworks, scope, regulatory focus, and disclosure philosophies. For cross-border companies or those reporting locally and globally, these differences shape not only reporting obligations but also the core of business operations.

Scope and Authority: J-GAAP, IFRS, US GAAP

Examining these three frameworks reveals how their underlying philosophies influence daily accounting and strategic decisions:

- J-GAAP is governed by the Accounting Standards Board of Japan (ASBJ) and is mandatory for most Japanese public companies. The ASBJ develops standards subject to endorsement by the Financial Services Agency (FSA), maintaining Japan's unique domestic regulatory framework.

- IFRS, under the International Accounting Standards Board, has been encouraged for listed companies in Japan on a voluntary basis since 2010. As of 2025, over 280 listed companies have adopted or plan to adopt IFRS, representing roughly 42% of TSE market capitalization.

- US GAAP applies to SEC registrants and is overseen by the Financial Accounting Standards Board. A small number of Japanese companies cross-listed in the United States continue to report under US GAAP.

- IFRS is principle-based, allowing management more judgment, while US GAAP and J-GAAP are rule-based and more prescriptive. This distinction has practical implications for how teams document decisions and prepare for audits.

- Japan uniquely permits four accounting frameworks for listed company reporting: J-GAAP, IFRS, US GAAP, and Japan's Modified International Standards (JMIS) -- a system unmatched by any other major economy.

- Selecting the appropriate standard early is critical for startups and lean teams to avoid expensive revisions as the organization grows.

Statutory Books and Group Reporting Boundaries

A key distinction lies in how reporting boundaries are defined. In Japan, statutory reporting is primarily focused on the legal entity, requiring strict preparation and retention of statutory books under J-GAAP. This influences audits, tax treatments, dividend calculations, and internal controls. By contrast, IFRS and US GAAP define a group more broadly, consolidating subsidiaries based on governance and economic substance. According to PwC Japan, IFRS often includes joint ventures and structured entities not consolidated under J-GAAP. Consequently, a Japanese subsidiary's books can differ greatly from what global headquarters expects, leading to discrepancies in profits, asset values, and group ratios. For global teams, careful alignment of statutory, internal, and group reporting is essential to prevent mismatches during closings or audits.

Materiality Philosophy and Disclosure Approach

Materiality and disclosure requirements differ significantly between J-GAAP and IFRS. Japanese standards mandate minimum specified disclosures and are generally more prescriptive. In contrast, IFRS adopts a principle-based approach, granting management discretion to determine investor-relevant materiality. The Accounting Standards Board of Japan observes that IFRS demands more judgment in applying materiality, whereas J-GAAP dictates minimum requirements. Teams risk under-disclosure (leading to regulatory scrutiny) or over-disclosure (leading to inefficiency). The key takeaway: systems must support judgment and robust documentation to meet international investor expectations and ensure both compliance and credibility.

| Area | J-GAAP | IFRS | US GAAP |

|---|---|---|---|

| Framework Approach | Rule-based, prescriptive | Principle-based, judgment-driven | Rule-based, highly detailed |

| Goodwill Treatment | Systematic amortization over up to 20 years | Annual impairment testing only | Annual impairment testing only (simplified option since ASU 2017-04) |

| Lease Accounting | Some leases remain off-balance sheet | Nearly all leases on balance sheet (IFRS 16) | Nearly all leases on balance sheet (ASC 842); distinguishes finance vs operating |

| Revenue Recognition | Industry-specific guidance, post-convergence alignment | Single five-step model (IFRS 15) | Single five-step model (ASC 606) with more implementation guidance |

| Credit Loss Model | Incurred loss model | Expected credit loss model (IFRS 9) | Current expected credit loss model (CECL); most front-loaded |

| Consolidation Scope | Legal entity focus; subs may report under other GAAPs | Broader economic substance and governance; no local GAAP flexibility | Variable interest entity model; primary beneficiary test |

| Disclosure Philosophy | Minimum prescribed disclosures | Management-judged materiality | Extensive rule-based disclosures; highest compliance burden |

| R&D / Development Costs | Generally expensed immediately | Capitalization permitted when IAS 38 criteria met | Expensed as incurred (ASC 730); software may be capitalized under ASC 350-40 |

| Fiscal Year Convention | March 31 predominant (~70% of listed cos.) | Flexible year-end, no prescribed period | Calendar or fiscal year; SEC filing deadlines (60/90 days) |

| Financial Statement Language | Japanese mandatory for statutory filings | Language of the jurisdiction | English for SEC filings |

Japan Reporting Pathways and Regulatory Implications

Foreign subsidiaries in Japan face dual obligations: mandatory J-GAAP statutory reporting for local compliance, plus conversion or reconciliation to their parent's IFRS or US GAAP framework for group consolidation -- making reporting pathway decisions among the most consequential for operational efficiency and cash flow.

For overseas founders and global companies, managing Japan's reporting landscape means reconciling statutory local requirements with global consolidation needs. Dual reporting, audit requirements, and structured dividend policies are just the beginning -- each choice in entity structure, bookkeeping, and reporting can have major compliance and cash flow implications.

Decision Flow for Subsidiaries and Branches

Determining the right approach for subsidiaries or branches in Japan involves several key steps:

1. Each legal entity incorporated in Japan must use J-GAAP for statutory reporting, regardless of foreign ownership.

2. Many global groups require their Japanese subsidiaries to provide reconciled or adapted financials under IFRS or US GAAP for group consolidation.

3. Startups and new market entrants need to establish systems and teams capable of managing both Japanese statutory requirements and timely conversion or reconciliation for group reporting.

4. These conversions and reconciliations are not optional; missing them can delay or halt consolidations, audits, or regulatory reviews.

5. Neglecting integrated reporting can result in cash flow constraints and miscommunication between local and global leadership.

Dual Books vs. Conversion Package Choices

To balance local and group requirements, companies choose between maintaining dual sets of books or preparing conversion packages. Full dual books under J-GAAP and IFRS/US GAAP provide control, but require significant investment. Most organizations prefer periodic conversion packages, mapping adjustments from J-GAAP to group standards at period-end. According to KPMG, dual bookkeeping is costly, often prompting companies to opt for reconciliation packages. Regardless of approach, consistency, firm version control, and clear communication between Japanese and head office finance teams are crucial for accuracy and audit readiness. For startups, scalable processes for conversion improve agility as the reporting environment grows more complex.

Audit, Attestation, and Filing in Japan

Auditing requirements in Japan are strict and extend beyond just listed companies. Under the Companies Act and Financial Instruments and Exchange Act, public companies and certain large private entities must undergo statutory audits by licensed auditors. The Japanese Institute of Certified Public Accountants (JICPA) oversees the profession and sets auditing standards that align with International Standards on Auditing while incorporating Japan-specific requirements. These audits focus on J-GAAP financials, or IFRS when used for group consolidation. Statutory filings are heavily regulated, and timely submission of audited accounts is mandatory to ensure stakeholder transparency. Efficient, precise, and well-documented accounting processes are essential -- especially when dealing with multiple frameworks. Global teams should note that audits and filings are mandatory in Japanese, essential for upholding trust and credibility in the Japanese market. For a deeper look at filing obligations, see our Japanese tax filing and compliance guide.

Dividend Capacity and Legal Reserves

Profit distributions in Japan are tightly linked to statutory financials and legal reserve requirements. Dividend capacity under J-GAAP is based on measured retained earnings, with mandatory allocations to legal reserves. Before paying dividends, companies must set aside these reserves to protect creditors and maintain stability. Even with higher profits under IFRS at the group level, a Japanese entity may have limited dividend capacity due to J-GAAP results or insufficient legal reserves. Deloitte points out that maintaining legal reserves is mandatory before dividends can be distributed. Founders and CFOs must coordinate finance functions at both local and global levels, especially where capital repatriation is a priority. Early awareness and planning are vital to avoid cash flow delays or shareholder misunderstandings.

Practical Implications for Foreign Subsidiaries

Foreign subsidiaries operating in Japan encounter specific practical challenges that go beyond theoretical framework differences -- from chart of accounts mapping and tax basis alignment to transfer pricing documentation and intercompany reconciliation workflows.

The theoretical differences between J-GAAP, IFRS, and US GAAP translate into tangible operational challenges for foreign subsidiaries operating in Japan. Understanding these practical implications helps finance teams plan systems, allocate resources, and avoid costly surprises during close periods and audits.

Chart of Accounts Mapping and System Configuration

Foreign subsidiaries must maintain a chart of accounts that satisfies both J-GAAP statutory requirements and group consolidation needs. This typically involves creating a mapping layer between the Japanese statutory chart of accounts and the parent's IFRS or US GAAP account structure. Key considerations include separate account codes for items treated differently under each framework (such as operating leases capitalized under IFRS 16 but kept off-balance sheet under J-GAAP), sub-accounts for goodwill amortization versus impairment tracking, and tagging mechanisms for items that require conversion adjustments. Many companies implement ERP tagging functions or parallel ledgers to facilitate dual reporting without maintaining fully separate books.

Tax Basis Alignment and Deferred Tax Differences

Japan's corporate tax calculations are based on J-GAAP financials, not IFRS or US GAAP figures. This creates deferred tax differences that require careful tracking. For example, goodwill amortized under J-GAAP generates tax-deductible expenses on a predictable schedule, while the same goodwill under IFRS carries no amortization charge until impairment occurs. Understanding tax depreciation categories and methods in Japan is essential for modeling these effects accurately. Lease capitalization differences also affect deferred tax balances, as the J-GAAP off-balance sheet treatment and the IFRS on-balance sheet right-of-use asset create different temporary differences. Teams must reconcile these across both frameworks at each reporting period, and the corporate income tax rate structure in Japan adds further complexity with national, prefectural, and municipal components.

Transfer Pricing and Intercompany Transactions

Cross-border intercompany transactions between a foreign parent and its Japanese subsidiary must be documented under both the parent's framework and J-GAAP. Revenue recognition timing differences between frameworks can affect intercompany profit elimination and transfer pricing outcomes. Companies should establish clear policies for intercompany pricing, ensure consistent recognition across frameworks, and maintain documentation that satisfies both Japanese tax authorities and the parent company's audit requirements. The National Tax Agency of Japan closely scrutinizes transfer pricing arrangements, particularly where framework differences might obscure the economic substance of intercompany flows.

| Disclosure Requirement | J-GAAP | IFRS | US GAAP |

|---|---|---|---|

| Segment Reporting | Required for listed cos.; aligned with IFRS 8 post-convergence | IFRS 8 management approach; extensive quantitative disclosure per segment | ASC 280; operating segments based on chief operating decision maker reporting |

| Related Party Transactions | Prescribed minimum disclosures; transactions with parent and subs | IAS 24; broader definition of related parties; key management compensation required | ASC 850; detailed disclosure of nature, amounts, and terms; compensation aggregated |

| Subsequent Events | Disclose material events through filing date | IAS 10; adjusting and non-adjusting events through authorization date | ASC 855; evaluate through date financial statements are available to be issued |

| Fair Value Measurement | Limited fair value hierarchy requirements | IFRS 13; three-level fair value hierarchy with extensive disclosure | ASC 820; three-level hierarchy; most detailed quantitative disclosure requirements |

| Earnings Per Share | Basic and diluted EPS required for listed companies | IAS 33; basic and diluted EPS on face of income statement | ASC 260; basic and diluted EPS; more detailed dilution methodology guidance |

| Contingent Liabilities | Disclose when probable; generally conservative recognition | IAS 37; probable = more likely than not; expected value measurement for large populations | ASC 450; probable = likely to occur; range of loss disclosure; more prescriptive thresholds |

| Operating Lease Commitments | Note disclosure of future minimum lease payments | On-balance sheet recognition; maturity analysis of lease liabilities required | On-balance sheet; maturity analysis; separate finance and operating lease tables |

| Sustainability / ESG | Voluntary; SSBJ standards under development | ISSB alignment (IFRS S1, S2) expected mandatory for listed cos. | SEC climate disclosure rules; scope 1 and 2 emissions for large accelerated filers |

Statutory Audit Requirements and Compliance Thresholds

Statutory audit obligations in Japan are triggered by company size thresholds under the Companies Act and securities regulation under the Financial Instruments and Exchange Act -- and the scope, timing, and language requirements differ materially from international audit norms.

Understanding exactly when and how statutory audits apply is essential for foreign companies establishing operations in Japan. The audit landscape is governed by multiple statutes, each with distinct thresholds and requirements that affect both listed and private entities.

Companies Act Audit Thresholds

Under the Companies Act, a company must appoint an independent auditor (kaikei kansanin) if it meets either of the following criteria: capital of 500 million yen or more, or total liabilities of 20 billion yen or more. These "large companies" (dai kaisha) must have their financial statements audited by a licensed CPA or audit firm registered with JICPA. Even companies that do not meet these thresholds may be required to appoint auditors if specified in their articles of incorporation. For Kabushiki Kaisha (KK) entities -- the most common structure for foreign subsidiaries -- the audit obligation is an important consideration during entity structure selection.

Financial Instruments and Exchange Act Requirements

Companies with securities listed on Japanese exchanges must file annual securities reports (yuuka shouken houkokusho) audited by registered audit firms. These audits follow Japanese auditing standards issued by the Business Accounting Council under the FSA, which are broadly aligned with International Standards on Auditing. The filing deadline is within three months of the fiscal year-end, and all filings must be prepared in Japanese. Companies that also report under IFRS for group consolidation must ensure that the IFRS-based financial statements included in securities reports are also subject to audit in accordance with Japanese standards.

Internal Controls Over Financial Reporting (J-SOX)

Japan's internal controls framework -- commonly called J-SOX -- requires listed companies to assess and report on the effectiveness of internal controls over financial reporting. Based on the US Sarbanes-Oxley Act but with Japan-specific modifications, J-SOX allows more flexibility in materiality settings and applies a risk-based approach. Companies reporting under both J-GAAP and IFRS must maintain internal controls that address the requirements of both frameworks, including controls over conversion adjustments and reconciliation processes. The management assessment report and the auditor's opinion on internal controls are filed alongside the annual securities report.

2025-2027 Changes: IFRS 18 and Sustainability Alignment

IFRS 18 (effective 2027) will restructure the income statement with mandatory operating, investing, and financing subtotals, while Japan's concurrent alignment with ISSB sustainability standards will expand corporate disclosure requirements into climate, governance, and supply chain risk areas.

International accounting and sustainability standards will increasingly shape Japanese corporate reporting in the years ahead. The introduction of IFRS 18 and alignment with ISSB standards signal a new era of transparency and comparability -- impacting not just reporting, but the management of key metrics and performance indicators across borders.

New Primary Statements and Required Subtotals

IFRS 18 brings significant updates to reporting frameworks, with these main impacts:

- IFRS 18 requires mandatory subtotals for operating, investing, and financing profits and losses in the primary statements, ensuring consistency and clarity.

- Companies must recategorize income statement and balance sheet items to meet the new presentation rules, enhancing transparency.

- Investors gain improved comparability across markets as standardized metrics replace previously subjective figures.

- Management faces greater accountability for reported results due to explicit, externally defined line items.

- Early adoption of IFRS 18 can help startups and lean companies demonstrate reliability and global readiness, boosting investor confidence and access to capital.

Management-Defined Performance Measures (MPMs)

IFRS 18 introduces formal rules for Management-Defined Performance Measures, establishing a standard for how companies present non-GAAP metrics:

- MPMs must be disclosed with clear definitions, methodologies, and reconciliations to IFRS line items.

- This transparency helps investors evaluate management claims against standardized benchmarks.

- Companies must carefully design internal systems to capture and report MPM data accurately.

- Deloitte observes that IFRS 18's MPM requirements will reduce ambiguity in financial reporting and increase the rigor of investor communications.

- Starting MPM preparation early allows companies to establish reliable reporting processes before mandatory adoption.

ISSB Sustainability and Climate Reporting Integration

Japan is aligning with ISSB standards (IFRS S1 and S2) for sustainability and climate reporting, expanding the scope of corporate disclosure. The Sustainability Standards Board of Japan (SSBJ) is localizing these standards to fit the Japanese market. The main impacts include:

- Companies must integrate sustainability reporting into existing financial reporting systems, not treat it as a separate exercise.

- Supply chain, environmental risk, and governance disclosures will be subject to regulatory review and auditor scrutiny.

- For global teams, aligning Japanese disclosures with international sustainability standards simplifies group reporting and builds stakeholder trust.

- Early investment in sustainability data collection and reporting infrastructure positions companies for compliance and competitive advantage.

Japan-Specific Convergence Timeline

Japan's convergence timeline continues to evolve, with chart of accounts management in Japan playing an integral role in these transitions. The Accounting Standards Board of Japan and the Financial Services Agency coordinate on converging J-GAAP with IFRS while preserving local regulatory priorities. Key milestones include expanded voluntary IFRS adoption, mandatory sustainability disclosures for listed companies, and ongoing updates to J-GAAP to align with international best practices.

Companies should proactively prepare for upcoming changes by consulting with auditors and legal advisors, building flexible reporting systems, and training finance teams to operate across standards. Staying ahead of these developments ensures smooth transitions, reduces compliance risk, and enhances competitive positioning in both Japanese and global markets. Tracking the Japan tax filing schedule and important dates helps teams coordinate reporting deadlines with broader compliance activities.

Transition Considerations: Moving Between Standards

Companies transitioning from J-GAAP to IFRS or managing a first-time adoption should expect a phased process spanning 6 to 12 months, with parallel reporting periods, system upgrades, and governance changes that require dedicated project leadership and cross-functional coordination.

For companies considering a transition from J-GAAP to IFRS -- whether driven by a parent company mandate, IPO preparation, or strategic investor relations goals -- the process involves far more than accounting policy changes. A successful transition requires coordinated effort across finance, IT, legal, and executive teams.

Gap Analysis and Project Scoping

The first step in any transition is a comprehensive gap analysis comparing current J-GAAP policies to target IFRS requirements. This assessment identifies areas where accounting treatments differ, systems require modification, and new data collection processes are needed. Common high-impact areas include lease reclassification (moving operating leases onto the balance sheet under IFRS 16), goodwill treatment conversion (ceasing amortization and implementing impairment testing), revenue contract reassessment under IFRS 15, and financial instrument reclassification under IFRS 9. Companies typically dedicate the first 90 days to this analysis, establishing a cross-functional project team and defining a clear timeline with milestones.

Parallel Reporting and Comparative Periods

IFRS first-time adoption requires at least one year of comparative financial data under IFRS. This means companies must run parallel J-GAAP and IFRS reporting for the comparative period, producing dual financial statements that are both auditable. PwC notes that this parallel reporting phase is the most resource-intensive part of the transition, often requiring temporary staffing, consultant support, and accelerated system configuration. The parallel period also serves as a testing ground for new processes, allowing teams to identify and resolve issues before the first fully IFRS-compliant reporting period.

System and Process Changes

IFRS adoption typically requires changes to ERP configurations, consolidation software, and reporting templates. Lease accounting modules must be upgraded or implemented to handle IFRS 16 right-of-use asset calculations. Revenue recognition modules need configuration for IFRS 15 performance obligation tracking. Chart of accounts must be expanded to accommodate IFRS-specific line items while maintaining J-GAAP statutory reporting capability. Training programs for finance staff -- including bilingual close procedures and IFRS technical updates -- are essential to sustain the transition beyond the initial implementation.

Frequently Asked Questions

Can a foreign subsidiary in Japan report only under IFRS and skip J-GAAP?

No. All legal entities incorporated in Japan must prepare statutory financial statements under J-GAAP for Companies Act compliance, tax filing, and dividend calculation purposes. Even if the parent company reports under IFRS globally, the Japanese subsidiary must maintain J-GAAP statutory books. The subsidiary can additionally prepare IFRS conversion packages or dual books for group consolidation, but J-GAAP statutory reporting cannot be bypassed.

How long does it typically take to transition from J-GAAP to IFRS?

A full transition typically takes 6 to 12 months, depending on the complexity of operations and readiness of existing systems. The process includes gap analysis (approximately 90 days), policy harmonization and system changes (90-180 days), and parallel reporting with dual close rehearsals (90-180 days). Companies with significant lease portfolios, complex revenue arrangements, or multiple subsidiaries should plan for the longer end of this range. Adequate financial and personnel resources are essential, as underestimating the effort often leads to delays and compliance risks.

What triggers a mandatory statutory audit in Japan?

Under the Companies Act, a statutory audit is required when a company has capital of 500 million yen or more, or total liabilities of 20 billion yen or more. Companies with securities listed on Japanese exchanges must also file audited annual securities reports under the Financial Instruments and Exchange Act. Even companies below these thresholds may be subject to audit requirements if specified in their articles of incorporation or if they are subsidiaries of listed groups subject to group audit procedures.

How does goodwill treatment affect dividend capacity for Japanese subsidiaries?

Since dividend capacity in Japan is determined by J-GAAP statutory financials, the systematic goodwill amortization under J-GAAP directly reduces retained earnings available for distribution. A subsidiary that has made acquisitions may show higher earnings under IFRS (where goodwill is not amortized) but have limited distributable capacity under J-GAAP due to accumulated amortization charges. This discrepancy is particularly important for foreign parents relying on dividends from Japanese subsidiaries as a capital repatriation mechanism.

Will IFRS eventually become mandatory in Japan?

As of 2026, IFRS remains voluntary for listed companies in Japan, and the FSA has not announced a mandatory adoption timeline. Japan's four-framework system (J-GAAP, IFRS, JMIS, US GAAP) continues to operate, though the trajectory of voluntary adoption and ongoing convergence efforts suggest continued movement toward IFRS alignment. The ASBJ continues to update J-GAAP to reduce differences with IFRS, and the growing number of adopters (over 280 listed companies, approximately 42% of TSE market cap) indicates a market-driven trend toward IFRS even without a regulatory mandate.

Conclusion

Bridging the gap between Japanese and international accounting standards is essential for any global team operating in Japan. Proactive planning, robust systems, and deep understanding of J-GAAP, IFRS, and US GAAP differences empower companies to achieve compliance, transparent reporting, and confident stakeholder engagement. By investing in localized knowledge, dual-reporting infrastructure, and ongoing training, international founders and finance teams can build a strong foundation for sustainable growth in Japan's dynamic business environment.

Yuga Koda is a founding Director at AQ Partners, supporting foreign companies, funds, and families operating in Japan. His experience operating companies in both Japan and international markets gives him a practical understanding of back office operations from both sides.